Submitted:

07 October 2025

Posted:

08 October 2025

You are already at the latest version

Abstract

This study examines whether the value, rarity, inimitability, and organisational support (VRIO) factors of artificial intelligence influence customers’ perspectives of artificial intelligence and the organisational performance of selected deposit money banks in Abuja. This study adopted a quantitative research method and utilised a cross-sectional research design to achieve its research objectives. The selected deposit money banks were Access Bank, First Bank, GT Bank, UBA Bank, and Zenith Bank. For this study, 136 customers from these five deposit money banks were sampled through a convenience sampling technique. Statistical Package for Social Sciences (SPSS) version 26 was utilised in conducting the non-parametric independent sample Kruskal-Wallis test that determines the statistical significance of this study, while the epsilon-squared effect size was used to ascertain the practical significance of this study. The findings indicated that the value, rarity, inimitability, and organisational support factors of artificial intelligence have significant influence customers' perspectives of artificial intelligence and the organisational performance of the selected deposit money banks in Abuja. Similarly, the epsilon-squared effect size indicated that the value, rarity, inimitability, and organisational support factors of artificial intelligence have small effect sizes on customers' perspectives on artificial intelligence and the organisational performance of the selected deposit money banks in Abuja. This study indicated that the VRIO factors of artificial intelligence have no significant influence on customers' perspectives of artificial intelligence and the organisational performance of the selected deposit money banks in Abuja.

Keywords:

VRIO

; artificial intelligence

; customers’ perspectives

; organisational performance

; deposit money banks

; Abuja

1. Introduction

1.1. Background to the Study

Artificial intelligence is a key factor in enhancing organisational performance. This assertion is centred on the belief that artificial intelligence improves operational efficiency through humans-to-technology interactions. According to Strykar and Kavlakoglu (2024), artificial intelligence (AI) is a technology that aids human learning by independently solving problems and improving decision-making. This implies that AI is designed to perform human tasks in today’s meta-verse transactions. For example, Graig, Laskowski, and Tucci (2025) explain that AI is a technology trained by humans to analyse patterns, make predictions, and engage in interactive communication using vast amounts of data. The performance of AI is determined by its factors. These factors of AI are its value, rarity, inimitability, and organisational support.

Frery (2024) defines the value factor of AI as the ability to use technology to increase the economic value an organisation generates by either increasing customers' willingness to pay for its services, reducing the costs of its services, or both. The rarity factor of AI refers to performance that is efficient and effective and is not common among other organisations within an industry. For instance, Barney and Clark (2007) argue that if the value factor of an organisation's resource or capability (such as in the context of AI) is possessed by many organisations, each organisation will exploit it. This will lead to common strategies that do not provide a competitive advantage among these organisations. Furthermore, Frery (2024) defined the inimitability factor of AI as the capability of the technology which are not replicable across organisations and is sustained through an organisation's history and corporate reputation among key players in its external environment (i.e., customers, suppliers etc.). According to Barney and Clark (2007), an organisation with a long history of adaptability to technological environment change is competitive compared to its competitors in the same industry. For the value, rarity, and inimitability factors of AI to enhance organisational performance, an organisation’s AI technology must garner organisational support from its different levels of management. For example, Barney and Clark (2007) note that the value, rarity, and inimitability factors of any resources or capabilities can only enhance sustained organisational performance if the organisation is properly structured. This includes the organisation’s formal reporting structures, management control systems, and compensation policies that enhance an organisation's potential for achieving organisational performance. Consequently, these value, rarity, inimitability, and organisational-support factors have metamorphosed AI into a global interest for public and business organisations.

In Europe, governments have realised that digital transformation by AI is a necessity for public organisations. This enables these organisations with the ability to deliver quality services to citizens and stakeholders (Misuraca, van Noordt, & Boukli, 2020). For example, Australia’s Taxation Office virtual assistant called “Alex” responds to more than 500 questions at a time. It has engaged in 1.5 million conversations and resolved over 81% of enquiries at first contact. However, business reports and empirical studies had, initially, argued that many European public and business organisations were struggling to leverage AI applications. This made it unclear how the factors of AI can be realised from AI investment and its influence on organisational performance (see Mikalef, Fjørtoft, & Torvatn, 2019). Currently, the European public and business organisations have tackled this uncertainty surrounding their struggle with their AI investment and its leverage on organisational performance. For instance, European banks have adopted real-time AI fraud detection technology to save their banks from 90% spoofing losses over the years (Digital Defynd, 2025). This indicates the role of the application of the value, rarity, inimitability, and organisational-support factors of AI in enhancing organisational performance is still a going concern.

In Africa, countries like South Africa and Kenya have adopted AI in both public and business organisations. This has enhanced both countries' public and business organisations' performance through the factors of AI. In the agricultural sector, for example, South Africa uses "ITIKI" machine learning technology to predict the propensity of droughts in its agricultural sector. Likewise, the Kenyan government's Forest Guards have adopted Microsoft's AI in mitigating illegal logging activities and tackling climate change. Furthermore, the Kenyan government uses "PlantVillageNuru", a state-sponsored machine learning AI, in helping farmers recognise farming plants' diseases. In the financial sector, South Africa's “Mama Money” and Kenya-based “M-KOPA” are AI technologies that enhance both countries' cybersecurity, customer experiences, and inclusive access to financial services (Convergence, 2025).

In Nigeria, deposit money banks (DMBs) have adopted AI as a resource to enhance organisational performance. Aliyu (2023) defines DMBs as financial institutions that accept money deposits from customers and provide low-interest loans to their customers. Therefore, the organisational performance of DMBs relies on reducing operating expenses and lowering risky bank transactions through the use of AI. For example, DMBs in Nigeria have seen a 63% increase in service efficiency and organisational performance due to the adoption of AI technologies (Ogundele et al., 2025). This lays the basis for studies on AI and the organisational performance of DMBs in Nigeria.

Recent studies by Okoliko et al. (2023) and Udodiugwu et al. (2024) demonstrate how AI enhances the efficiency, effectiveness, productivity, and enhancement of customer experience in tandem with DMBs’ organisational performance. The study was conducted through surveys of employees in DMBs in Nigeria. Additionally, Amado et al. (2024) and Olumoyegun, Alabi, and Nurudeen (2024) highlight that AI has a significant impact on the organisational performance of DMBs in Nigeria. Furthermore, studies agree that AI has an impact on the efficiency, effectiveness, innovation, risk management, and operational compliance, which translates to the operational performance of DMBs in Nigeria (Okoliko et al., 2023; Udodiugwu et al., 2024).

Nevertheless, these studies have failed to take into account customers’ perspectives of AI and the organisational performance of DMBs in Nigeria, which are differentiable based on the value, rarity, inimitability, and the organisational-support factors of AI. According to Kamba (2025), DMBs’ financial products or services are becoming increasingly similar. This has blurred the strategic significance of the factors of AI and the organisational performance of DMBs, which lean on differentiability. According to Kamba (2025), customers’ perspectives of the factors of AI are now the ultimate differentiator of DMBs' organisational performance. This entails customers’ expectations of personalised and seamless interactions across DMBs’ AI multiple channels (i.e., mobile banking, USSD, and WhatsApp banking). Furthermore, Kamba (2025) notes that DMBs that master the hyper-personalisation of customer services and prioritise customers will emerge as market leaders in today’s AI-driven financial industry.

Arguably, DMBs’ adoption of AI in Nigeria is still at the infant stage of AI's adoption maturity cycle. According to Price Water Coopers ([PWC], 2025), only 10 out of 26 DMBs in Nigeria have adopted AI to enhance customer engagement and customer service issue resolutions. As such, DMBs' value, rarity, inimitability, and the organisational-support factors of AI that enhance customers’ perspectives of the DMBs' organisational performance are yet to be ascertained. This highlights the nuance between the ideal customers’ perspectives of AI and the actual customers’ perspectives of AI and the organisational performance of DMBs in Nigeria. For example, Ibrahim and Adepoju (2023) claim that DMBs' customers lack trust in AI adoption. This scepticism is based on a lack of trust in AI accuracy, its inability to handle complex queries, and a lack of awareness of AI-driven financial services. Thus, DMBs' customers are more comfortable resolving banking issues through interactions with human agents rather than relying on AI-integrated banking services (Eze & Nwankwo, 2023).

1.2. Statement of the Problem

Currently, the influence of the factors of AI on customers’ perspectives of AI and the organisational performance of DMBs in Nigeria is still a new frontier. Studies are yet to investigate this issue. This indicates that the value, rarity, inimitability, and organisational-support factors of AI that influence customers’ perspectives of AI and the organisational performance of DMBs in Nigeria are yet unknown or under studied. Consequently, if left unknown or understudied, the knowledge of whether the value, rarity, inimitability, and organisational support of AI influence customers’ perspectives of AI and the organisational performance of DMBs in Nigeria will remain a subliminal challenge to AI’s strategic implementation and management. Thus, this creates a strategic question to be addressed: do the value, rarity, inimitability, and organisational-support factors of AI embedded in AI capability influence customers’ perspectives of AI and the organisational performance of DMBs in Nigeria? To address this strategic question, this study adopts resource based view's (RBV) value, rarity, imitability, and organisational support (VRIO) model to ascertain the factors of AI that influence customers’ perspectives of AI and the organisational performance of DMBs in Abuja, which will serve as a microcosm to a broad context of DMBs in Nigeria.

1.3. Objectives of the Study

To address the issues identified in the statement of problem, this study examines whether the VRIO factors of AI influence customers’ perspectives of AI and the organisational performance of DMBs in Abuja. Meanwhile, the specific objectives of this study are to:

- i.

- Determine if the value factor of AI has a significant influence on the organisational performance of selected DMBs in Abuja;

- ii.

- Assess if the rarity factor of AI has a significant effect on customers' perspectives of AI and the organisational performance of selected DMBs in Abuja;

- iii.

- Examine if the inimitability factor of AI has a significant impact on Customers’ perspectives of AI and the organisational performance of selected DMBs in Abuja;

- iv.

- Lastly, investigate if the organisational-support factor of AI have a significant impact on customers' perspectives of AI and the organisational performance of selected DMBs in Abuja.

1.4. Research Questions

In response to the research questions above, this study posits the following hypotheses.

- i.

- Does the value factor of AI have a significant influence on customers' perspectives of AI and the organisational performance of selected DMBs in Abuja?

- ii.

- Does the rarity factor of AI have a significant effect on customers' perspectives of AI and the organisational performance of selected DMBs in Abuja?

- iii.

- Does the inimitability factor of AI have a significant impact on customers' perspectives of AI and the organizational performance of selected DMBs in Abuja?

- iv.

- Lastly, does the organisational-support factor of AI has a significant impact on customers' perspectives of AI and the organisational performance of selected DMBs in Abuja?

1.5. Research Hypotheses

In response to the research questions above, this study posits the following hypotheses.

- i.

- H01: The value factor of AI has no significant influence on customers' perspectives of AI and the organisational performance of selected DMBs in Abuja.

- ii.

- H02: The rarity factor of AI has no significant effect on customers' perspectives of AI and the organisational performance of selected DMBs in Abuja.

- iii.

- H03: The inimitability factor of AI has no significant impact on customers' perspectives of AI and the organisational performance of selected DMBs in Abuja.

- iv.

- H04: The organisational support factor of AI has no significant influence on customers' perspectives of AI and the organisational performance of selected DMBs in Abuja.

1.6. Significance of the Study

This study helps understand the VRIO factors of AI that influence, or do not influence, customers’ perspectives of AI and the organisational performance of selected DMBs in Abuja. Furthermore, this study provides DMBs' marketing departments with the importance of the VRIO model in analysing customers' perspectives of AI and organisational performance. Finally, this study gives insight into customers’ perspectives of AI as a strategic resource and capability that will influence the sustainability of the organisational performance of the selected DMBs in Abuja.

1.7. Scope of the Study

In tandem with this study's narrative above, the scope of this study encompasses customers of five DMBs located in Abuja, the Federal Capital Territory. Specifically, this study focuses on customers of DMBs that have integrated AI into their operations. The selected customers of the DMBs for this study are customers banking with Access Bank, First Bank, Guaranty Trust Bank (GTBank), United Bank of Africa Bank (UBA Bank), and Zenith Bank (ref., Nwokoji, 2023). Furthermore, this study concentrates on examining the influence of the RBV’s VRIO factors of AI on customers’ perspectives of AI and the organisational performance of selected DMBs in Abuja.

Thus, the subsequent sections of this study are structured as follows. Section 2 presents the literature review. Section 3 outlines the research method employed by this study. Section 4 presents the findings of this study. Lastly, section 5 presents the discussion, conclusions, and recommendations of this study.

2. Literature Review

As previously mentioned in the introduction, AI has a significant impact on the organisational performance of DMBs. However, operational risks persist in customers’ perspectives of the organisational performance of DMBs in Nigeria. While previous studies have focused on AI and organisational performance from the organisation-centric perspective (i.e., management and employees’ perspectives) of DMBs in Nigeria, this study examines whether the factors of AI influence customers' perspectives on AI and the organisational performance of selected DMBs in Abuja. To achieve this goal, this study utilised the RBV theory and customer expectancy motivation theory to examine the impact that the value, rarity, inimitability, and organisational support factors of AI have on customers’ perspectives of AI and the organisational performance of selected DMBs in Abuja. Subsection 2.1 introduces the conceptual framework of this study, while subsections 2.2 and 2.3 delve into the theoretical review and the analysis of empirical studies relevant to this study, respectively.

2.1. Conceptual Framework

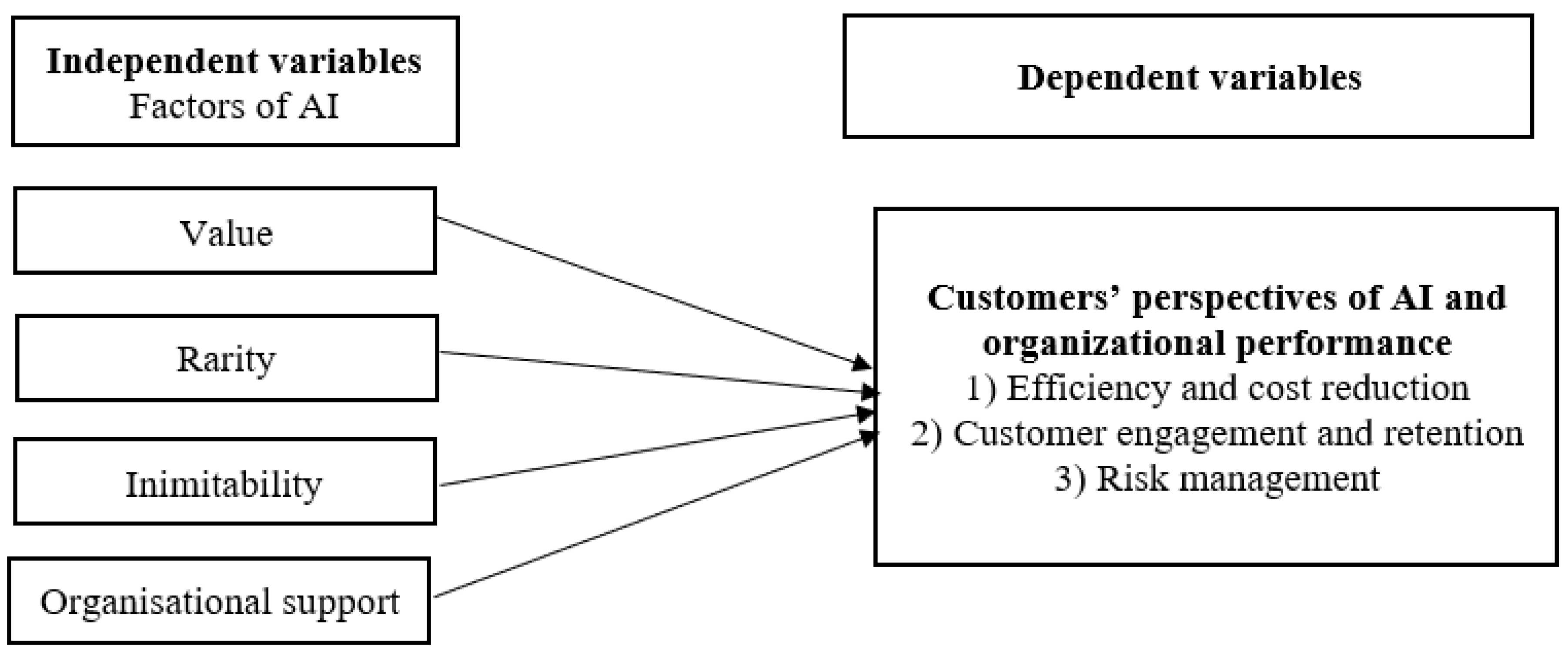

Figure 1 illustrates the connections between decoupled VRIO value factors of AI that influence customers’ perspectives of AI and the organisational performance of selected DMBs in Abuja.

2.1.1. Value Factor of Artificial Intelligence and Organisational Performance

The value factor of AI and organisational performance refer to an organisation's capacity to reduce operational costs and increase profitability; ultimately, leading to enhanced customer satisfaction. This factor of AI influences the organisational performance of DMBs through process automation, cost reduction, improved risk assessment, and lower default rates (Bellefonds et al., 2024). From the customers' perspectives, the value factor of AI represents the perceived benefits derived from the services of DMBs. This is based on customers' recognition of the functional and economic value of AI and DMBs' organisational performance. The functional value factor of AI pertains to how well AI meets customers' practical needs, while the economic value factor of AI emphasises the cost reductions in DMBs' transactions that customers experience. Despite the value factor of AI and organisational performance among DMBs, the rarity factor of AI determines how the value factor of AI influences customers' perspective of DMBs' organisational performance (Mei et al., 2024).

2.1.2. Rarity Factor of Artificial Intelligence and Organisational Performance

The rarity factor of AI and organisational performance refer to the uniqueness of the factors of AI within an industry. When an organisation possesses a rare factor of AI, it generates more functional and economic value than its competitors. The rarity factor of AI impacts organisational performance when its applications are unique among DMBs, creating more value for customers compared to competitors in the industry. However, if many DMBs adopt similar value factor of AI, their rarity factor of AI will not contribute to organisational performance (Frery, 2024). Therefore, the rarity factor of AI and organisational performance are defined by their unique applications among DMBs. Notably, customers will perceive the rarity factor of AI through service efficiency and differentiation. Despite the value and rarity factors of AI and organisational performance of DMBs, its inimitability factor is sacrosanct.

2.1.3. Inimitability Factor of Artificial Intelligence and Organisational Performance

The inimitability factor of AI and organisational performance refer to the difficulty in replicating an organisation's factors of AI. For the factors of AI to enhance organisational performance, it must be challenging for competitors to imitate (Frery, 2024). The inimitability factor of AI impacts organisational performance by deterring competitors from easily replicating existing factors of AI across DMBs. From a consumer's perspective, the imitability factor of AI will be difficult for customers to differentiate another competitors' factors of AI. This increases the cost of the factors of AI awareness. Conversely, inimitable factors of AI will reduce customers' expected costs during customer-to-AI transactions. To ensure the effectiveness of the inimitability factor of AI, there must be an organisational support system for the factors of AI to enhance organisational performance.

2.1.4. Organizational Support Factor of Artificial Intelligence and Organizational Performance

The organisational support factor of AI and organisational performance involves leveraging the factors of AI to enhance organisational performance. This includes effective management control, compensation policies, and strategic planning to maximise organisational performance (Frery, 2024). Customers perceive the organisational support factor of AI and the organisational performance of DMBs through an organisation's management, customisation of customer experiences, automation of operations, result-oriented risk management, and overall operational performance. Consequently, the interplay between value, rarity, inimitability, and organisational support factors determine how customers perceive the factors of AI and the organisational performance of DMBs.

2.2. Theoretical Framework

2.2.1. Resource-Based View (RBV) Theory

The Resource-Based View (RBV) theory is a strategic management paradigm that explains how organisations achieve and maintain competitive advantages by effectively utilising their unique internal resources or factors. This theory explains how an organisation outperforms its competitors within an industry. The resource-based view (RBV) theory highlights and predicts the influence of value, rarity, inimitability, and organisational support on an organisation’s organisational performance and competitive advantage among strategic groups. According to Barney and Clark (2017), organisational performance improves when an organisation maximises its internal strengths and minimises its weaknesses by utilising its current resources or factors. Likewise, Barney and Clark (2007) opined that organisations must possess resources or factors that are valuable, rare, inimitable, and have organisational support. Without these qualities, an organisation's resources or factors will struggle to achieve its intended organisational performance, as well as sustainable competitive advantage.

2.2.2. Customers' Expectation Motivation Theory

Customers' expectation motivation theory revolves around an individual's anticipated outcome of an event, situation, or performance based on their past experiences. Customers anticipate the results of an event, situation, or performance based on their own experiences or other sources of information. For instance, Oliver (2010) notes that customers’ expectations involve comparing an organisation's promised benefits with its actual performance. Therefore, customers' expectations of organisational performance are influenced by post-transaction experience or offers from business competitors (Kotler & Keller, 2012).

According to Mulyani and Fitrianti (2012), customers' expectations are primarily influenced by enduring service intensifiers, implicit service promises, past experiences, and personal needs. Enduring service intensifiers encompass customers' overall expectations of organisational performance, including the gap between their ideal and actual organisational performance. For instance, customers using a logistics service would expect fast and convenient delivery as a standard for organisational performance. These enduring service intensifiers are essentially implied service promises made by an organisation. Furthermore, implicit service promises serve as the criteria customers use to assess organisational performance. Parasuraman, Zeithamul, and Berry (1987) observed that customers evaluate an organisation's product or service performance based on the promised benefits. Thus, customers’ final evaluation depends on whether the organisation delivered its promised benefits or not. As a result, customers' past experiences depend on an organisation's implicit product or service promises.

2.3. Empirical Review

Okoliko et al. (2023) investigated AI and organisational performance of selected DMBs in Nigeria. The study utilised a cross-sectional descriptive research design and a structured survey questionnaire. A total of 135 employees from five selected DMBs in Abuja participated in the study. Statistical analysis was conducted using the Statistical Package for Social Sciences (SPSS) version 22 to run multiple regression analyses on the data. The main findings of the study revealed that AI significantly increased the efficiency, effectiveness, productivity, customer satisfaction, and the overall organisational performance of the selected DMBs.

Salemcity, Aiysan, and Japine (2023) studied AI adoption and the corporate operating activities of DMBs in Nigeria. The study adopted an ex-post facto research design. The findings showed that AI adoption had a negative effect on employee costs, while it had a positive effect on the operating systems of DMBs in Nigeria.

Ofuani, Omoera, and Akagha (2024) examined the integration of AI and the organisational performance at the United Bank of Africa, Nigeria. The study collected primary data from 130 employees and analysed its data with Pearson's correlation. The study found that robotic process automation AI had a significant impact on the bank's organisational performance, while Chatbot and customer service systems did not have a significant effect on the organisational performance of the DMB.

Chinwendu, Enudu, and Orga (2024) investigated AI and the organisational performance of DMBs in the Southeastern region of Nigeria. The study focused on the influence of cardless automated teller machines (ATM) on employee retention and the impact of point-of-sale terminals on loss prevention. The study utilised a survey design research approach and collected primary data from 271 employees in the region. The data was analysed using Pearson's correlation test. The study revealed that cardless ATMs had a significant influence on employee retention, while point-of-sales terminals had a positive significant effect on loss prevention in DMBs in the Southeastern part of Nigeria.

Udodiugwu et al. (2024) studied the role of AI in enhancing the organisational performance of DMBs in Nigeria. The study showed that AI in customer services improved the non-financial organisational performance of DMBs, while strong cybersecurity AI enhanced their financial organisational performance. The study focused on Access Bank, Fidelity Bank, Guaranty Trust Bank, and First Bank of Nigeria, while utilising SPSS version 23 for its statistical analysis.

Adepeju et al. (2024) examined AI and risk management of DMBs in Nigeria. The study adopted a survey research design. The study reported that AI had a significant impact on GT Bank's credit scoring and enhanced fraud detection in the risk management of DMBs.

Olumoyegun, Alabi, and Nurudeen (2024) investigated the contemporary issues on AI and the performance of selected DMBs in Nigeria. The study adopted a cross-sectional research design. The findings indicated that Chatbots and robotic advising systems had a significant effect on employees' operational performance.

Unuesiri and Adejuwon (2024) investigated the effect of an AI expert system on the financial performance of DMBs in Abuja. The study adopted a longitudinal research design, which encompassed Access Bank, Zenith Bank, UBA Bank, and GT Bank's AI adoption from 2015-2023. The findings pointed out that the AI expert system has both positive and significant effects on the operational performance of DMBs in Abuja.

Ogundele et al. (2025) analyse the impact of AI on sustainable banking and service delivery in DMBs in Nigeria. The study included 384 DMBs' customers from Access Bank, Fidelity Bank, Guaranty Trust Bank, and Zenith Bank. The study adopted Jarque Beta, correlation analysis, and ordinary least squares. The findings indicated that AI awareness, application, and effectiveness influenced the services of the selected DMBs in Nigeria.

Lastly, Orjinta and Anetoh (2025) investigate how AI strategies lead to sustainable performance of DMBs in Nigeria. The study utilised an ex-post facto research design to ascertain these DMBs' operational activities from 2014-2023. The findings suggested that AI had a significant effect on the sustainable performance of DMBs in Nigeria.

2.3.1. Appraisal of Reviewed Literature

This study’s appraisal of the reviewed literature is threefold. First, the theoretical framework forms the foundation of this study. Second, the limitations of empirical studies on AI and the organisational performance of DMBs’ research designs are identified. Lastly, the significance of the VRIO model in attaining this study's objectives.

First, Mulyani and Fitrianti's (2012) factors influencing customers' expectations service (such as service intensifiers, implicit service promises, past experiences, word of mouth, and personal needs) are most relevant to this study. These customer expectations explain the VRIO factors of AI that influence customers' perspectives of AI and the organisational performance of selected DMBs in Abuja. Additionally, these customers’ expectation factors indicate how the VRIO factors of AI align with customers' perspectives of AI and the organisational performance of the selected DMBs in Abuja.

Second, empirical studies on AI and organisational performance among DMBs in Nigeria have primarily focused on efficient and effective organisational performance (Okoliko et al., 2023; Ofuani, Omoera, & Akagha, 2024; Udodiugwu et al., 2024) and employee retention (Chinwendu, Enudu, & Orga, 2024). Except for Ogundele et al.’s (2025) study, which focused on AI and the organisational performance of DMBs in Nigeria from customers’ perspectives. Furthermore, the empirical studies' findings have been based on DMBs' management and employees' perspectives. Notably, Ogundele et al. (2025) highlight customers' perspectives of AI technology and its effect on organisational performance of DMBs in Nigeria. The study suggests that studies on AI and organisational performance of DMBs in Nigeria are organisation-centric. Furthermore, the findings of these studies are limited by their research designs. These limitations result from a lack of statistical power to ascertain the effect of AI and the organisational performance of DMBs in Nigeria. For example, the ex-post facto research design adopted by Salemcity, Aiysan, and Japine (2023) as well as Orjinta and Anetoh (2025) does not have the capacity to assign research respondents into groups to ascertain each group's unique perspectives on their research topics. As a result, respondents will be obliged to give favourable responses. Similarly, Unuseri and Adejewon's (2024) longitudinal research design does not encompass customers' perspectives of AI and the organisational performance of DMBs in Nigeria.

Lastly, the VRIO factors of AI (adopted from the RBV concept) provide a model to determine which factors of AI are heterogeneous and not transferable across DMBs to create sustainable organisational performance of DMBs in Nigeria. Although the VRIO model has not been tested in the context of AI and the organisational performance of DMBs in Nigeria, the model has proven its significance in determining how the VRIO factors of DMBs' resources impact their competitive parity (i.e., to maintain or defend a current position without the intent to outperform competing firms within a strategic group) and competitive advantages. For example, Simamara, Rahayu, and Dirgantari (2024) used the VRIO model to ascertain the competitive parity of DMBs' human resources, organisational structure, and products and services. Likewise, the model helped determine the competitive advantages of DMBs' capital resources, information systems, and organisational reputation in Pakistan.

All in all, the value, rarity, inimitability, and organisational support factors of AI indicate how DMBs' organisational performance is differentiated. Similarly, from the customers' perspectives of AI, the value, rarity, inimitability, and organisational support factors of AI will arguably indicate some dimension of organisational performance of the selected DMBs in Abuja.

3. Methodology

This study adopted a quantitative research method. The quantitative research method was adopted because of its effectiveness in testing hypotheses and theories through statistical analysis (Kumar, 2019). Additionally, this study adopted a quantitative research method because of the objectivity of its procedures and the comparability of its results across studies (Walsh, 2024).

3.1. Research Design

In addition to the quantitative research method adopted, this study utilised a cross-sectional research design. The cross-sectional research design was adopted because of its ability to observe the variables within data without influencing them or establishing a cause-and-effect relationship between variables (Thomas, 2023). Furthermore, the cross-sectional research design is crucial to this study because it allows for the observation of preliminary information over time for subsequent studies (Babbie, 2008).

3.2. Population of the Study

This study’s sample population comprised the customers who bank with one or more of the selected DMBs in Abuja, FCT. The selected DMBs were Access Bank, First Bank, GT Bank, UBA Bank, and Zenith Bank in Abuja, FCT.

3.3. Sample and Sampling Techniques

This study's sample size was 136 customers of the selected DMBs in Abuja. These customers were selected by a non-probability convenience sampling technique. The non-probability convenience sampling technique was adopted because of its adequacy in a situation where available data on a population are not available (Sekaran & Bougie, 2016). Furthermore, this sampling technique was adopted for its cost-effectiveness and efficiency in situations where there is no predetermined sample population or sample frame (Kumar, 2019; Leavy, 2017).

3.4. Instrument of Data Collection

This study adopted a survey questionnaire in its data collection. The survey questionnaire was chosen for its simplicity in gathering data not easily accessible through secondary sources (Leavy, 2017). To protect the interests and personal information of the respondents who participated in this study, the survey questionnaire included an informed consent slip outlining the author’s title, the protection of respondents' information, and the voluntary participation of respondents.

The survey questionnaire consisted of 19 items structured into five sections: A, B, C, D, and E. Section A (7 items) focused on respondents' demographics, including gender, number of accounts with selected banks, awareness of AI applications, and platform interactions. Sections B to E (12 items) related to the VIRO constructs of the study, were measured on a five-point Likert scale, which was scaled from 1 = Strongly Disagree (SD) to 5 = Strongly Agree (SA).

3.5. Validity of the Instrument

Principal Component Analysis (PCA) was used to evaluate the construct validity of the survey questionnaire in this study. Construct validity determines if a test accurately measures what it claims to measure (Ghaza et al., 2020). PCA was performed on the 12 items in the survey questionnaire. The Kaiser-Meyer-Olkin (KMO) measure confirmed that the study had adequate sampling for the analysis, with a KMO value of 0.69 and significance at a P-value of .001, which indicated that the sample size of this study is adequate (Kaiser, 1974).

3.6. Reliability of Instrument

The survey questionnaire underwent a Cronbach's alpha reliability test to ensure internal reliability and homogeneity across the construct. The Cronbach Alpha reliability scores of the four components of this study were as follows. The value capability of the AI construct had a Cronbach's Alpha score of .804. The rarity capability of AI, consisting of 5 items, had a Cronbach's Alpha score of .827. The inimitability of AI, with 2 items, had a Cronbach's Alpha of .792. Finally, the organisational support capability of AI, with 3 items in its construct, had a Cronbach's Alpha score of .841 (see Appendix, p. 25). All of these scores were above the Cronbach Alpha reliability score of .70 (Cronbach, 1951; Taber, 2017).

3.7. Procedure of Data Collection

The data were gathered through a self-administered questionnaire from random respondents in workplaces and at automated teller machine (ATM) locations of the selected DMBs in Abuja. The data collection procedure involved four steps. First, respondents were approached and asked for their consent to participate in this study. The respondents were informed about the study's purpose and were provided with informed consent. Second, the distribution and collection of filled survey questionnaires were based on respondents' convenience some preferred to fill and return the questionnaires immediately. However, some respondents requested more time to complete them beyond the initial timeframe. Nonetheless, this study's data collection had a seventy-eight per cent (78%) response rate.

3.8. Method of Data Analysis

This study utilised the services of Statistical Package for Social Science (SPSS) version 26 to conduct both descriptive and inferential statistics. Descriptive statistics were used to categorise respondents according to their bank account operations with the selected DMBs in this study. For ease of data analysis, the data collected on each variable of the VIRO construct were transformed into single individual variables. For example, the two variables under the value factor of AI were transformed into a single variable value.

Consequently, an independent sample Kruskal-Wallis non-parametric test was used to conduct the inferential statistics. This study adopted the Independent sample Kruskal-Wallis non-parametric test because it is ideal for measuring ordinal data. Furthermore, this study found the Independent sample Kruskal-Wallis non-parametric test ideal because of its ability to analyse the interactions between three or more independent variables and dependent variables. The VRIO factors of AI are the independent variables, while the customers' perspectives of AI and organisational performance are the dependent variables. This is important because the VRIO model presents a practical framework that is easy to comprehend and utilise (Kaliannan et al. 2023). The model offers a comprehensive approach to identifying the critical factors of AI that influence customers' perspectives of AI and the organisational performance of the select DMBs in Abuja. Additionally, it distinguishes resources that offer short-term benefits and those that are sustainable (Barney and Hesterly, 2012).

In addition to the adopted Independent sample Kruskal-Wallis non-parametric test, this study also adopted epsilon squared (E2) to determine the effect sizes of variance between customers' perspectives of organisational performance explained by the VRIO factors of AI (Lee, 2025; Bobbitt, 2021). The inferential statistics were based on a 95% confidence interval and a P-value of .05. A P-value greater than .05 will retain the null hypotheses of this study, while a P-value less than .05 will reject the null hypotheses of this study.

Regarding the epsilon squared effect size, the effect size was calculated manually using the formula:

E2 = (H – K + 1) / (n–k)

Where:

H = Kruskal-Wallis H statistics;

K = the number of groups under observation;

n = the total number of observations.

As a rule of thumb, the small effect size is between .01 and < .06. A medium effect size falls within the range of .06 and < .14, while a strong effect size falls above .14 (Tomczak & Tomczak, 2014).

4. Results and Discussion

4.1. Data Presentation

Before proceeding with the analysis of this study's findings, it is essential to consider the demographic characteristics of the respondents sampled in this study. The respondents comprised customers from Access Bank, First Bank, GT Bank, UBA Bank, and Zenith Bank. The respondents were categorised based on the following criteria: gender, primary DMB for transactions, the number of DMB accounts held, alternative DMBs utilised for transactions, awareness of AI integration in the selected DMBs’ operations, and the specific AI platforms utilised by the selected DMBs they patronised.

4.1.1. Demographic Characteristics of Respondents

Table 1 indicates that 56 respondents (41.2%) identify as male, while 80 respondents (58.8%) identify as female. 36 respondents (26.5%) reported having only one bank account with the selected DMBs in Abuja. 100 respondents (73.5%) indicated they maintain multiple bank accounts across the selected DMBs in Abuja. 63 respondents (46.3%) reported having no alternative bank accounts among the selected DMBs in Abuja.

In terms of alternative banking transactions with the selected DMBs in Abuja, Access Bank respondents represented 6.6% of the sample population, while First Bank accounted for 2.9% of the sample population. Additionally, 18.4% of respondents from UBA Bank and 15.4% from GT Bank reported having alternative bank accounts with other selected DMBs in Abuja. Furthermore, 14 respondents (10.3%) from Zenith Bank also reported similar alternative banking transactions with the selected DMBs in Abuja.

In terms of respondents’ awareness of AI in banking transactions and various platforms with selected DMBs in Abuja, it was found that 76 respondents (55.9%) were aware of AI applications in the selected DMBs' transactions, while 32 respondents (23.5%) were unaware. 28 respondents (20.6%) were uncertain of AI in the banking transactions of the selected DMBs in Abuja, respectively.

Concerning the use of AI-integrated banking platforms by the selected DMBs in Abuja, 28% of the respondents utilised DMBs' AI-integrated web pages during banking transactions with the selected DMBs in Abuja. 25.7% of the respondents used AI-integrated WhatsApp platforms by the selected DMBs in Abuja. Lastly, 27.2% of the respondents accessed DMBs' applications on the Google Play Store, while 19.1% interacted with chatbots during their transactions with the selected DMBs in Abuja.

4.2. Testing of Hypotheses

To test this study's hypotheses, an independent sample Kruskal-Wallis test and epsilon-squared effect size were utilised in analysing the statistical and practical significances of this study (see Table 2).

The following hypotheses were tested to achieve the objectives of this study.

4.2.1. Hypothesis One

H01: The value capability of AI has no significant influence on customers' perspectives of AI and the organisational performance of selected DMBs in Abuja. The Kruskal-Wallis test indicated that the value capability of AI has no significant influence on customers' perspectives of AI and the organisational performance of the selected DMBs in Abuja, with H(4) = 7.02, p-value = .13, and E2 = .02.

4.2.2. Hypothesis Two

H02: The rarity capability of AI has no significant effect on customers' perspectives of AI and the organisational performance of selected DMBs in Abuja. The Kruskal-Wallis test demonstrated that the rarity capability of AI has no significant effect on customers’ perspectives of AI and the organisational performance of the selected DMBs in Abuja, with H(4) = 7.23, p-value = .12, and E2 = .03.

4.2.3. Hypothesis Three

H03: The inimitability capability of AI has no significant impact on customers' perspectives of AI and the organisational performance of selected DMBs in Abuja. The Kruskal-Wallis test revealed that the inimitability capability of AI has no significant impact on customers' perspectives of AI and the organisational performance of the selected DMBs in Abuja, with H(4) = 1.70, p-value = .79, and E2 = -.02.

4.2.4. Hypothesis Four

H04: The organisational-support capability of AI has no significant influence on customers' perspectives of AI and the organisational performance of selected DMBs in Abuja. Similarly, the Kruskal-Wallis test indicated that the organisational-support capability of AI has no significant influence on customers' perspectives of AI and the organisational performance of the selected DMBs in Abuja, with H(4) = 8.28, p-value = .08, and E2 = .03.

4.3. Discussion

The results of this study indicated that the value, rarity, inimitability, and organisational support factors of AI had no significant effect on customers’ perspectives or the overall organisational performance of the DMBs examined in Abuja. This result corroborates the assertions of Barney and Clark (2017) and, more recently, Frery (2024), who contended that factors of AI lacking genuine rarity, value, or inimitability will not facilitate sustainable organisational performance. This discussion examines the findings through the VRIO dimensions.

- i.

- Value factor of AI: Customers' perspectives of AI were not influenced by the value factor of AI (convenience, enquiries, and trustworthy information feedback). Instead of seeing these services as novel or unique, customers perceived this factor as a component of the standard DMBs' package. Their expectations may already have been shaped by service assurances, industry norms, and previous interactions with these selected DMBs. This is in line with the findings of Ofuani, Omoera, and Akagha (2024), who also found that AI-driven customer service systems has no significant effect on DMBs' organisational performance. Customers of DMBs often complain about inefficiencies, so it makes sense to assume that the convenience factor of AI would be more important. However, the undervaluation of the value factor of AI by consumers indicated the lack of customer recognition of AI tools’ actual value addition to the selected DMBs' organisational performance in Abuja.

- ii.

- Rarity factor of AI: The rarity factor of AI, which included unique offerings, timely and accurate responses, and management commitment, also did not affect customers' perspectives of AI and organisational performance of the selected DMBs in Abuja. Hence, customers perceived no rarity factor of AI. Thus, this indicates customers perceived AI homogeneity across the selected DMBs in Abuja. This is contrary from Okolioko et al.’s (2023) findings, which found that AI had a significant positive impact on the organisational performance of DMBs. This disparity begs the question of whether Abuja consumers are less aware of AI than those in the Okolioko et al. (2023) study regions. Hence, customers may lack the exposure necessary to identify variations in AI implementation and how they affect DMBs' organisational performance in Abuja.

- iii.

- Inimitability factor of AI: Customers' perspectives of AI and the organisational performance of the selected DMBs were unaffected by AI's inimitability factors, such as distinctive services and corporate reputation. Consumers believed that these AI-related products were not a source of competitive organisational because they were simple to imitate. This demonstrates a possible flaw in the way DMBs position or brand their AI initiatives. This validates the third hypothesis of the study. This is one of the most obvious conclusions: the selected DMBs' AI brands are hard to differentiate.

- iv.

- Organisational-support factor of AI: Lastly, customers did not consider the organisational support factor of AI (which includes cost reduction, engagement, retention, and efficiency) to be significant. This is in contrast to Okolioko et al. (2023), who discovered that the adoption of AI increased the DMBs' efficiency and satisfaction. Internal benefits and customer visibility seem to be at odds in this case. At the service level, customers may not always benefit from the cost savings or process improvements that the selected DMBs may be bringing about.

Overall, the data points to a largely generic adoption of AI by the selected DMBs in Abuja. The AI applications that are currently in use are not seen by customers as having strong value, rarity, inimitability, or organisational support. The long-term viability of AI adoption in the industry is affected by this. AI may enhance internal procedures from an organisation-centric perspective. However, from the customers' perspective, AI tools don't really stand out from the other DMBs that were selected in this study. This study's main finding was the disparity between the customer perspective and internal efficiency gains. It implies that AI in DMBs, at least in Abuja, is still primarily a back-office tool rather than an innovation that interacts strategically with customers.

5. Conclusion

This study examined whether customers' perspectives of AI and the organisational performance of selected DMBs in Abuja are impacted by the VRIO factors of AI. The findings demonstrated that there was no significant impact from any of the four factors of AI (value, rarity, inimitability, and organisational support). According to the organisation-centric perspective of DMBs, AI is now a standard feature for cost reduction and risk management. However, from the consumers' perspectives, AI is seen as neither special nor useful in meeting their banking expectations. Unarguably, customers are still DMBs' lifeblood. Nonetheless, AI's contribution to organisational performance will be limited if it does not meet customer expectations. This makes the findings of this study a new frontier. This implies that although the selected DMBs may celebrate improvements in internal efficiency, customers' banking expectations are yet to be met.

Therefore, AI must be more than just a service tool if it is to actually improve organisational performance. Visible customer benefits, awareness, and differentiation are essential. If not, AI will continue to function as a background efficiency mechanism that has no effect on customer loyalty or how an organisation is perceived to be performing. According to this study's findings, DMBs need to approach AI as a component of their customer strategy as well as a technology. The expectational gap between DMBs and their customers will continue to exist in the absence of a change in AI adoption, differentiation, and knowledge transfer strategies.

6. Recommendations

Based on the findings and discussion of this study, the following recommendations are made.

- i.

- Use VRIO as a benchmark: DMBs should use the VRIO model as a scorecard to determine whether their AI services actually offer customers recognisable service value, rare customer services, inimitable product and service offers, and organisational support. Without this kind of benchmarking, DMBs might keep spending money on AI without knowing if their customers will notice or value the changes in banking technology innovation.

- ii.

- Customise AI applications: DMBs should modify their AI tools to meet particular client needs rather than implementing generic AI systems. Instead of considering all services to be the same, this could assist customers in associating specific problem-solving skills with specific DMBs. The unexpected discovery that consumers viewed AI tools similarly across all chosen DMBs led directly to this recommendation.

- iii.

- Make brand positioning stronger: AI ought to be incorporated into the brand identity and reputation of every DMB. When customers perceive that an AI tool embodies a bank's distinct identity, it becomes more difficult for competitors to copy. This is an investment for the long run. As this study made clear, customers hardly ever connected AI tools to a particular DMB's brand.

- iv.

- Integrate AI into company culture: Knowledge of AI should be disseminated throughout departments, not just customer service, through internal marketing and training. Customer-facing services can better match internal capabilities when the entire organisation comprehends and strategically applies AI. This suggestion is in line with this study's finding that technical teams in DMBs tend to have the majority of the AI expertise, leaving other units out of the loop.

6.1. Limitations

Notably, the findings of this study's generalisation are encumbered by the following limitations.

- i.

- The sample population of the customers of five (5) selected DMBs in Abuja does not give a proper representation of the selected DMBs' branches' customers' perspectives of AI and their organisational performance across Nigeria.

- ii.

- Again, the 136 respondents that participated in this study and the non-probability convenience sampling technique adopted by this study do not give an adequate sample size that gives a significant representation of customers' perspectives of AI and the organisational performance of the selected DMBs in Abuja.

6.2. Suggestions for Further Studies

In tandem with the recommendations and the limitations of this study, the following suggestions for further studies are made.

- i.

- Sampling strategy: A larger range of customer viewpoints could be captured by using stratified or cluster sampling, which might show more pronounced patterns than this study did. Despite its usefulness, the current sample did not accurately represent the range of customer experiences in Abuja. Richer insights might be obtained with a more multi-layered approach.

- ii.

- Sample size: Greater statistical significance and more accurate testing of effect sizes would be possible with larger samples. The analysis indicated multiple times that a larger sample could have revealed effects that are noticeable here.

- iii.

- Scope: To get a more accurate picture of AI adoption by DMBs in Nigeria, the study should be expanded beyond the five selected DMBs in Abuja to include additional organisations and states. Abuja was the sole focus of this study, which now seems to have been a limited perspective. A more comprehensive national perspective would result from expanding to other states.

- iv.

- Specific indicators: Future research could use an AI–Customer Satisfaction Index or an AI Service Equity Index, for instance, to measure performance more precisely. These would make it possible to track the effects of the VRIO factors of AI on customers’ perspectives more precisely. Although this study adopted VRIO factors of AI as a metric, more focused indices could improve subsequent studies' findings.

Appendix

Reliability Test of Research Instrument

| Construct/ Items | Cronbach’s Alpha |

|

Value factor of AI 1. AI enhances the overall convenience of banking services. 2. AI enhances banking enquiries by providing reliable information. |

.804 |

|

Rarity factor of AI 3. AI is unique and not widely available across DMBs. 4. AI gives accurate feedbacks that are rare among DMBs. 5. AI is efficient and timely and is not common among DMBs. 6. DMBs’ management are committed to supporting AI initiatives. 7. DMBs’ employees are well trained to assist effectively with AI transactions. |

.827 |

|

Inimitability factor of AI 8. DMBs' operations are old enough to utilise capabilities of AI that is differentiable. 9. AI capability marches DMBs' corporate reputation among their customers. |

.793 |

|

Organizational-support factor of AI 10. DMBs have performed well in overall service efficiency and cost reduction. 11. DMBs have performed well in overall customers’ engagement and customer retention. 12. DMBs have performed well in overall fraud prevention and transaction risk management. |

.841 |

Source: Author’s SPSS computation, 2025.

References

- Adepeju, A. A. , Logunleko, S. D., Amusa, B. O., & Onifade, H. O. (2024). Artificial intelligence and risk management of deposit money banks: Empirical evidence of Guaranty Trust bank. Umyu Journal of Accounting and Finance Research, 7(1), 178-193. [CrossRef]

- Aliyu, A. A. (2023). Credit risk management and financial performance of deposit money banks in Nigeria. International Accounting and Taxation Review, 9(1), 17-29.

- Amado, A. I. , Emubor, R. O., Mogue, T. O., & Abudullahi, S. A. (2024). The impact of artificial on organisational performance: insights from VFD micro-finance banks, Lagos State, Nigeria. International Journal of Research and Innovation in Social Sciences (IJRISS), VII (XIV), 518-524. [CrossRef]

- Babbie, E. (2008). The basics of social research (4th Ed). Belmont, CA: Thomson Wadsworth.

- Barney, J.B. Firm Resources and Sustained Competitive Advantage. J. Manag. 1991, 17, 99–120. [Google Scholar] [CrossRef]

- Barney, J. B. , & Clark, D. N. (2007). Resource-based theory: Creating and sustaining competitive advantage. New York, NY: Oxford University Press.

- Barney, J. B. , & Hesterly, W. S. (2012). Strategic management and competitive advantage. USA: Pearson International Edition Prentice-Hall.

- Barney, J. B. , & Clark, D. N. (2017). Resource-based theory: Creating and sustaining competitive advantage. New York, NY: Oxford University Press.

- Bellefonds, N. D. , Frank, M. R., Forth, P., Luther, A., Lukic, V., & Nopp, C. (2024). Where is the value in AI? Boston Consulting Group (BCG).

- Chinwendu, A. M. , Enudu, T. O., & Orga, J. I. (2024). Artificial intelligence and organisational performance of banks in South-East Nigeria. Advanced Journal of Business and Entrepreneurship Development, 8(6), 23-48.

- Convergence. (25). 2025 quarter 1 AI in Africa summary report: Policy digital transformation, and capacity building. https://www.convergenceai.io. 20 April.

- Cronbach, L.J. Coefficient alpha and internal structure of tests. Psychometrika 1951, 16, 297–334. [Google Scholar] [CrossRef]

- Digital Defynd. (2025). 15 ways AI is being used in Europe. https://www.digitaldefynd.com/IQ/ways-ai-used-europe/.

- Eze, M. & Nwankwo, L. (2023). Human-machine collaboration in Nigerian banking: The future of AI chatbots. Journal of Digital Business, 9(1), 13-29.

- Frery, F. (2024). When artificial intelligence turns strategic resources into ordinary resources. ESCP Research Institute of Management (ERIM), 1-6.

- Ghaza, F. B. , Ramlee, S. N. S., Alwi, N., & Hizau, H. (2020). Content validity and test-retest reliability with principal component analysis of the translated Malay four-item version of the Paffenbarger Physical Activity Questionnaire. Journal of Health Research, 35(6), 493-505. [CrossRef]

- Graig, L. , Laskowski, N., & Tuuci, L. (2025). What is AI? Artificial intelligence explained. https://www.techtarget.com/searchenterpriseai/definition/AI-artficial.

- Ibrahim, T. , & Adepoju, R. (2023). The impact of AI chatbots on banking customer service in Nigeria. West African Journal of Financial Studies, 10(2), 78-96.

- Kaiser, H.F. An index of factorial simplicity. Psychometrika 1974, 39, 31–36. [Google Scholar] [CrossRef]

- Kaliannan, M.; Darmalinggam, D.; Dorasamy, M.; Abraham, M. Inclusive talent development as a key talent management approach: A systematic literature review. Hum. Resour. Manag. Rev. 2022, 33. [Google Scholar] [CrossRef]

- Kamba, E. (2025). 2025 industry trends: Insights from Africa's business leaders. The Board Room Africa. https://www.theboardroomafrica.com.

- Kotler, P. , & Keller, K. L. (2016). Marketing Management. Boston: Pearson.

- Kumar, R. (2019). Research methodology: A step-by-step guide for beginners. S: Thousand Oaks, CA.

- Leavy, P. (2017). Research Design: Quantitative, qualitative, mixed-method, art-based, and community-based participatory research approaches. New York: The Guilford Press.

- Mei, H.; Bodog, S.-A.; Badulescu, D. Artificial Intelligence Adoption in Sustainable Banking Services: The Critical Role of Technological Literacy. Sustainability 2024, 16, 8934. [Google Scholar] [CrossRef]

- Mikalef, P.; Fjørtoft, S.O.; Torvatn, H.Y. (2019). Developing an Artificial Intelligence Capability: A Theoretical Framework for Business Value. In W. Abramowicz, & R. Corchuelo (Eds.), Business Information Systems Workshops. [CrossRef]

- Misuraca, G.; van Noordt, C.; Boukli, A. The use of AI in public services. ICEGOV 2020: 13th International Conference on Theory and Practice of Electronic Governance. LOCATION OF CONFERENCE, GreeceDATE OF CONFERENCE; pp. 90–99.

- Mulyani, A, & Fitrianti, E. (2012). Analysis of the effect of customer expectations, product quality, and customer Satisfaction on credit card user loyalty. PT. XYZ, Tbk in Makasar. Hasanuddin University.

- Nwokoji, C. (2023, ). Seven banks compete in artificial intelligence adoption. Nigerian Tribune. https://amps/tribuneng.com/seven-banks-compete-in-artificial- intelligence-adoption/amp/. 3 January.

- Ofuani, A. B. , Omoera, C. I., & Akagha, C. (2024). Artificial intelligence and performance of money deposit banks in Lagos metropolis: A study of United bank of Africa. UniLag Journal of Business, 10(1), 54-81.

- Ogundele, A. T. , Ibitoye, O. A, Akinteiwa, O.A., Adeniran, A., Ibukun, F. O., & Apata, T. G. (2025). The role of artificial intelligence in advancing sustainable service efficiency in Nigeria. Journal of Sustainable development law and policy, 16 (1).

- Okoliko, E. O. , Ayetigbo, O. A., Ifegwu, I. J., & Chidiebere, N. U. (2023). Artificial Intelligence Impact in Revolutionising the Nigerian banking industry: An assessment of selected deposit money banks in Abuja. Achievers Journal of Scientific Research, 5(2), 120-131.

- Olumoyegun, P M., Alabi, J. O., & Nurudeen, Y. Z. (2024). Contemporary issues of AI and performance of employees at selected deposit money banks in Lagos, Nigeria. Journal of Business, Innovation, and Creativity, 3(2), 141-151.

- Orjinta, H. I. , & Anetoh, J. C. (2025). Achieving sustainable performance of deposit money banks in Nigeria through artificial intelligence strategies. Innovations, 80.https://journal-innovation.com.

- Parasuraman, A. , Zeithaml, V., & Berry, L. (1985). "A Conceptual model of service quality and its implications for future research. Journal of Marketing, 9-20.

- PWC. (2025). AI in Nigeria: Opportunities, challenges, and strategic pathways. https://www.pwc.com/ng.

- Salemcity, A.; Aiyesan, O.; Japinye, A.O. Artificial Intelligence Adoption and Corporate Operating Activities of Deposit Money Banks. Eur. J. Accounting, Audit. Finance Res. 2023, 11, 17–33. [Google Scholar] [CrossRef]

- Simamora, S.; Rahayu, A.; Dirgantari, P.D. Driving Digital Transformation in Small Banks With VRIO Analysis. J. Apl. Bisnis dan Manaj. 2024, 10, 99–99. [Google Scholar] [CrossRef]

- Strykar, C. , & Kavlakoglu, E. (2024, ). What is artificial intelligence (AI)? IBM.COM. https://www.ibm.com/think/topics/artificial/-intelligence?utm_source=perplexity. 4 August.

- Taber, K.S. The Use of Cronbach’s Alpha When Developing and Reporting Research Instruments in Science Education. Res. Sci. Educ. 2018, 48, 1273–1296. [Google Scholar] [CrossRef]

- Thomas, L. (2023). Cross-sectional study: Definition, uses, and examples. https://www.scribbr.com/method%20on%20May%208%2C%202020%20by%20Lauren,design%20ich%20you%20collect%20data%20from.

- Tomczak, M. , & Tomczak, E. (2014). The need to report effect size estimates: An overview of some recommended measures of effect size. Trends in Sports Sciences, 1 (21), 19-25.

- Udodiugwu, M. I. , Eneremadu, K. E., Onunkwo, A. R., & Gloria, O. C. (2024). The role of artificial intelligence in enhancing the performance of banks in Nigeria. Arabian Journal of Business and Management Review, 11(2), 27-34.

- Unuesiri, F. , & Adejuwon, J. A. (2024). Artificial intelligence expert system and financial performance of deposit money banks in Nigeria. International Institute of Academic Research and Development, 10(9), 39-54. [CrossRef]

- Walsh, G. (2024). Qualitative vs. quantitative research. Gwl.com. Retrieved from https://www.gwl.com/blog/qualitative-vs-quantitative/03fhs_amp=true.

Figure 1.

VRIO factors of AI that influence customers’ perspectives of AI and the organisational performance of selected DMBs in Abuja.

Figure 1.

VRIO factors of AI that influence customers’ perspectives of AI and the organisational performance of selected DMBs in Abuja.

Table 1.

Demographic Characteristics of Respondents.

|

Access Bank n % |

First Bank n % |

GT Bank n % |

UBA Bank n % |

Zenith Bank n % |

Full sample N % |

|

|

Gender Male Female Total |

24 50 24 50 48 100 |

10 62.5 6 37.5 16 100 |

15 39.5 23 60.5 38 100 |

2 20 8 80 10 100 |

5 20.8 19 79.2 24 100 |

56 41.2 80 58.8 136 100 |

|

Number of acct owned One acct More than one acct Total |

11 22.9 37 77.1 48 100 |

5 31.3 11 68.7 16 100 |

7 18.4 31 81.6 38 100 |

5 50 5 50 10 100 |

8 33.3 16 66.7 24 100 |

36 26.5 100 73.5 136 100 |

|

Alternative acct owned None Access Bank First Bank GT Bank UBA Bank Zenith Bank Total |

18 37.5 0 0 3 6.3 15 31.3 4 8.3 8 16.7 48 100 |

4 25.0 3 18.8 0 0 3 18.8 3 18.8 3 18.8 16 100 |

17 44.7 0 0 0 0 3 7.9 15 39.5 3 7.89 38 100 |

7 70 2 20 1 10 0 0 0 0 0 0 10 100 |

17 70.8 4 16.6 0 0 0 0 0 0 3 12.5 24 100 |

63 46.3 9 6.6 4 2.9 21 15.4 25 18.4 14 10.3 136 100 |

|

Type of acct Saving Current Fixed Total |

32 66.7 11 22.9 5 10.4 48 100 |

13 81.3 3 18.7 0 0 16 100 |

27 71.1 11 28.9 0 0 38 100 |

5 50 5 50 0 0 10 100 |

19 79.2 2 8.3 3 12.5 24 100 |

96 70.6 32 23.1 8 5.9 136 100 |

|

AI awareness Yes No Uncertain Total |

32 66.7 6 12.5 10 20.8 38 100 |

8 50 8 50 0 0 16 100 |

22 57.9 15 39.5 1 2.6 38 100 |

5 50 3 30 2 20 10 100 |

9 37.5 0 0 15 62.5 24 100 |

76 55.9 32 23.5 28 20.6 136 100 |

|

AI platform Chatbot Webpage Total |

14 29.2 12 25.0 9 18.8 13 27.0 48 100 |

2 12.5 2 12.5 3 18.7 9 56.3 16 100 |

5 13.2 18 47.4 7 18.4 8 21.0 38 100 |

2 20 3 30 3 30 2 20 10 100 |

3 12.5 2 8.3 13 54.2 6 25.0 24 100 |

26 19.1 37 27.2 35 25.7 38 28.0 136 100 |

Source: Author’s SPSS computation, 2025.

Table 2.

Independent-Sample Kruskal-Walis Test and Epsilon- Squared Effect Size's Results.

| P-Value | H-Statistics | Decision | Effect Size (E2) | |

| Value factor of AI | .13 | 7.02 | Retain null hypothesis | 0.02 |

| Rarity factor of AI | .12 | 7.23 | Retain null hypothesis | 0.03 |

| Inimitability factor of AI | .79 | 1.70 | Retain null hypothesis | -0.02 |

| Organisational support factor of AI | .08 | 8.28 | Retain null hypothesis | 0.03 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2025 by the author. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Copyright: This open access article is published under a Creative Commons CC BY 4.0 license, which permit the free download, distribution, and reuse, provided that the author and preprint are cited in any reuse.