Submitted:

04 July 2025

Posted:

07 July 2025

You are already at the latest version

Abstract

This study analyzes the application of International Accounting Standard IAS 41 – Agriculture in poultry companies (ISIC A0146.03) in the province of Tungurahua, Ecuador, with the aim of evaluating the degree of regulatory compliance, the level of technical knowledge of accounting managers and the impact of the lack of homogenization on the presentation of financial statements. The research is based on a quantitative-descriptive approach, through the application of a structured questionnaire to 26 representatives of poultry companies, complemented by the financial analysis of the activity during the period 2010–2024. The results show that the application of IAS 41 is not comprehensive or uniform, and various valuation methods are used that are not always aligned with the fair value approach required by the standard. Likewise, significant heterogeneity in accounting criteria is detected, which limits comparability and reduces the usefulness of financial information for decision-making. Most of the respondents have general but limited knowledge of the standard, which affects its technical implementation. The study concludes that it is necessary to strengthen specialized accounting training, establish sectoral standardization criteria and promote regulatory supervision to ensure transparent, coherent and useful financial information.

Keywords:

IAS 41

; biological assets

; poultry sector

; fair value

; agricultural accounting

1. Introduction

The agricultural sector represents an essential component in the Ecuadorian economy, not only because of its contribution to the Gross Domestic Product (GDP), but also because of its capacity to generate employment and food supply (CFN, 2024). Within this sector, poultry farming oriented to egg production (ISIC A0146.03) stands out for its dynamism and expansion, especially in provinces such as Tungurahua, where activity has grown significantly in recent years (CONAVE, 2021). This productive evolution demands more accurate and normatively aligned accounting systems that allow the financial and economic situation of poultry companies to be faithfully reflected (INEC, 2020).

In this context, International Financial Reporting Standards (IFRS) and in particular IAS 41 – Agriculture, play a key role in establishing technical guidelines for the recognition, measurement and presentation of biological assets (International Accounting Standard, 2017). The standard promotes the use of fair value minus estimated costs at the point of sale as a valuation basis, with the aim of providing useful, understandable, and comparable financial information (Carrión et al., 2021; Wen-hsin Hsu et al., 2019). However, its application presents particular challenges in biological activities such as the production of laying birds, where biological transformation is constant and often difficult to quantify in monetary terms.

In developing countries such as Ecuador, the practical adoption of IAS 41 has not been homogeneous, and empirical evidence on its implementation in specific sectors such as poultry is still limited (Fernandes et al., 2016). The lack of technical training, the lack of standardization of accounting criteria, and the particular conditions of the production environment contribute to a partial or inadequate application of the standard, which compromises the quality of financial statements and their usefulness for strategic decision-making (Chávez et al., 2023; Sedláček, 2014).

The main objective of this study is to analyze the application of IFRS in companies in the poultry sector of Tungurahua, identifying the prevailing accounting practices, the valuation methods used, and the perception of the owners or accounting managers regarding the impact of this regulation on the quality of financial information. Consequently, this article not only provides empirical evidence on the degree of compliance with IAS 41 in the Ecuadorian poultry sector, but also raises the need to strengthen training, regulation and accounting technology processes as a way to achieve greater transparency and efficiency in the financial management of this productive sector.

This research is beneficial both for the business sector and for accounting, regulators and academic professionals linked to agricultural accounting. It contributes to the design of technical training policies aimed at improving regulatory application in small and medium-scale enterprises. For watchdogs and regulatory bodies, the findings allow us to identify implementation gaps that need to be addressed with more effective sectoral supervision and regulation strategies. Finally, this study also adds value to the academic community, since it expands the theoretical-empirical body on agricultural accounting in emerging economies, and can serve as a basis for comparative research or for the development of accounting models adjusted to local contexts.

The study is organized into the following sections: (i) Introduction, (ii) Theoretical Framework, (iii) Materials and Methods, (iv) Results, (v) Discussion, (vi) Conclusions, and (vii) References.

2. Theorical Framework

2.1. Biological Active Ingredients and Their Typology

Biological assets are living resources, whether animals or plants, that entities manage for productive, transformation, or sale purposes (Osipchuk et al., 2024). Its definition, according to International Accounting Standard 41 (IAS 41), is framed in agricultural activities, understood as the management of biological processes to generate agricultural products or new biological assets (Nurunnabi, 2021). Biological transformation includes growth, degeneration, production, and procreation, which implies that assets are constantly changing in value, radically differentiating themselves from traditional fixed assets (Ifeanyieze et al., 2021).

From an accounting perspective, according to Hadiyanto et al. (2018), two main types are recognized:

- Consumable biological assets: intended to be harvested or slaughtered, such as chickens for meat or short-cycle crops.

- Biological production assets: those that generate income over time without being consumed directly, such as laying hens or fruit trees.

In the context of the Ecuadorian poultry sector, biological assets range from live animals in different stages of development, to products generated by them, such as eggs, chicks, or even by-products such as guano or secondary proteins (ACCA Global, 2024; Valverde et al., 2022). This diversity introduces complexities in their classification, valuation and accounting control, even more so when there are heterogeneous practices in companies, many of which do not apply the same regulatory criteria (Ning et al., 2022). In addition, poultry farming has a high degree of specialization and short production cycles, which requires an agile, dynamic accounting record aligned with the biological reality of the asset, which makes the correct application of international standards even more relevant (Rodrigues et al., 2025).

2.2. Fair Value and Accounting Treatment

One of the most discussed conceptual axes within IAS 41 is the use of fair value as the main basis for the initial and subsequent measurement of biological assets (Hinke, 2014). Fair value is defined as the price that would be received for selling an asset in an orderly transaction between market participants on the measurement date (Majercakova & Skoda, 2015). From this, the estimated costs at the point of sale are deducted, generating net value.

The subsequent measurement of the assets, according to the standard, must also be conducted based on this value, with the changes in its magnitude recognized in the results of the year. In certain cases, where it is not possible to measure fair value reliably, it is permitted to use the adjusted historical cost model, with the application of depreciation and impairment (Biondi & Oulasvirta, 2023; Guidolin, 2011).

In Ecuadorian practice, this approach has significant limitations, small and medium-sized poultry enterprises lack standardized measurement systems, and often do not have access to markets with representative prices. Research such as that by Bangsheng et al. (2020) and Hadiyanto et al. (2018) shows that, under these conditions, entrepreneurs prefer to use the historical cost due to its greater traceability, even if it does not faithfully reflect the economic reality of the biological asset.

However, studies have shown that the implementation of fair value can increase international comparability, tax accuracy, and efficiency in decision-making, generating added value in strategic management (Watkiss, 2019; Wang et al., 2021).

2.3. Regulatory Application in the Poultry Sector

The application of IAS 41 in the poultry sector is still incipient and uneven. International regulations establish general principles, but its practical operationalization requires specific adaptations that respond to the nature of poultry production (Menglikulov et al., 2024), where the stages of breeding, growth, laying, slaughtering and marketing can change over time and have different values depending on the species. the age of the bird, the feeding system, and other biological factors (Arimany et al., 2013).

Recent studies indicate that only a small percentage of poultry companies formally apply standardized valuation methods (Biljon & Wingard, 2020). This reflects not only low regulatory adoption, but also a lack of accounting training, absence of financial culture, and weakness in internal governance.

At the same time, other research such as that of Wudhikarn et al. (2025) suggests that the internal policies of each company play a determining role in the way IAS 41 is applied. Some companies opt for fair value only at the sale stage, while others apply it from early stages, generating heterogeneous financial results even within the same subsector (Bolzani, 2020). This situation raises the need for a flexible valuation model, adapted to the Ecuadorian context, which respects the guidelines of IAS 41 but allows to overcome existing structural barriers, such as informality, lack of technical knowledge or the lack of integrated accounting systems.

2.4. The Role of Accounting in Decision-Making Within the Agricultural Sector

Accounting, as a comprehensive financial information system, has a direct impact on the formulation of business, tax and strategic decisions. Its proper implementation generates reliable data for planning, monitoring, and evaluating economic and productive performance (Poljašević et al., 2019).

A critical aspect is the valuation of biological assets, whose accounting treatment affects the determination of the financial result, tax obligations, budgets, cash flow projections and the attraction of investments (Kurniawan et al., 2014). IAS 41 Agriculture requires that such assets be measured at fair value with less costs to sell, which improves the accuracy and transparency of financial statements (IAS, 2022).

The rigorous application of IAS 41 strengthens the reliability and comparability of accounting information, favoring access to financing and the formalization of strategic alliances, in addition to ensuring tax compliance (Hadiyanto et al., 2018; Nakasone & Castillo, 2023).

At the level of operational improvement, the recognition and accurate measurement of biological assets make it possible to know the real value of resources, manage production risks (health, climate, financial) and optimize internal processes. Studies show that companies that implement IAS 41 increase their transparency and market relevance, especially when they adequately disclose valuation levels(M. da Silva et al., 2015). The standard also provides guidelines for land-linked assets (such as planted trees), allowing the use of methods such as residual: total value minus value of land, adjusting for the highest and best use according to IFRS 13. Authors such as Nuhu et al. (2021) and Silva et al. (2024) highlight that the incorporation of modern accounting criteria, such as fair value and activity-based costing (ABC), favors greater production efficiency, waste reduction, and alignment between real costs and market prices, critical factors in the economic sustainability of the agricultural sector.

3. Materials and Methods

3.1. Research Approach and Design

This research adopts a quantitative approach, with a non-experimental design and descriptive-analytical scope, aimed at examining the application of accounting standards in the valuation of biological assets within the poultry sector, specifically in companies registered under ISIC code A0146.03 (Egg production) in the province of Tungurahua, Ecuador. The study set out to identify accounting practices, business perceptions and the degree of alignment with the International Accounting Standard through financial information from secondary sources and the application of structured data collection instruments.

3.2. Population and Sample

The population was composed of poultry companies active in Tungurahua, identified through records of the Internal Revenue Service (SRI) and the Superintendence of Companies, Securities and Insurance. The sample was non-probabilistic of an intentional type, made up of 26 companies whose representatives voluntarily agreed to participate in the study. These key actors have direct knowledge about the accounting and financial management processes in their organizations.

3.3. Data Collection Tools and Techniques

A structured questionnaire composed of closed and multiple-choice questions was designed and applied, focused on five key dimensions: (1) normative knowledge, (2) valuation methods applied, (3) accounting criteria for biological assets, (4) treatment of the poultry production cycle and (5) usefulness of financial information for decision-making. The instrument was validated by the judgment of experts in financial accounting.

In addition, secondary accounting and financial data (assets, liabilities, equity, net local sales, income, costs and expenses) were collected from official sources such as the Internal Revenue Service (IRS) from its SAIKU 2.0 data viewer. in the period 2010–2024, in order to contextualize the financial situation of the sector in the province analyzed, its evolution and relationship with the valuation of biological assets.

3.4. Data Processing and Analysis

To contextualize the study from a macro perspective, an exploratory analysis of economic activity ISIC A0146.03 was conducted at the national level, using information published by official entities such as the SRI. The provinces with the highest participation in terms of total assets, local net sales (0% rate) and profit for the year were identified, which allowed a comparative ranking to be established. From this analysis, it was concluded that the province of Tungurahua leads in the three key variables, positioning itself as one of the most representative authorities of the poultry sector in Ecuador.

Consequently, this province was selected to carry out a detailed analysis of its accounting and financial information, covering the period 2010–2024, which was represented by descriptive graphs that reflect the evolution of indicators such as assets, liabilities, equity, income, costs and expenses, in order to obtain a comprehensive view of the financial and economic behavior of the sector and its relationship with the accounting application of biological assets.

The data of the questionnaire were processed using descriptive statistics (frequencies and percentages), which allowed the identification of patterns and trends in the application of accounting regulations. At the same time, a table of relevant results was constructed by question with their respective analysis and interpretation.

As a qualitative and semantic complement, a keyword concurrence diagram was developed from the textual analysis of the responses and their interpretation, using text mining techniques and visualization of semantic networks using Python software and specialized libraries such as scikit-learn and networkx. This tool allowed the identification of the strongest conceptual relationships between the key terms used, reinforcing the coherence of the technical discourse around the valuation of biological assets.

3.5. Research Question

Within the framework of this research, the main question arises: How are the accounting standards for the valuation of biological assets applied in companies in the poultry sector (ISIC A0146.03) of Tungurahua, and what is the perception of their owners regarding their impact on financial information and decision-making? This question allows us to investigate not only the degree of technical application of accounting regulations, but also the assessment made by business actors on their practical usefulness. To delve deeper into this problem, three specific sub-questions were formulated:

- Q1: Are the International Financial Reporting Standards (NIFF) fully applied in the accounting record of biological assets in companies in the poultry sector in Tungurahua?

- Q2: What level of technical knowledge do the owners or accountants have about IAS 41 and how does it influence its practical application?

- Q3: How does the lack of homogenization affect the application of accounting standards on the presentation and comparability of financial statements in companies in the poultry sector (ISIC A0146.03) of Tungurahua?

These questions guided the methodological design and the analysis of the results, allowing a comprehensive understanding of the challenges and opportunities represented by the adoption of accounting standards in production environments with high biological intensity.

3.6. Ethical Considerations

The confidentiality and anonymity of the participants was guaranteed, informing them in advance of the academic purposes of the research. All participants provided their informed and voluntary consent for data collection and analysis.

4. Results

The presentation of the results begins with a sectoral diagnosis that allows contextualizing the current state of the poultry sector in Ecuador and Tungurahua, specifically in the economic activity classified under ISIC code A0146.03, corresponding to the production of poultry eggs. This analysis is essential to understand the productive dynamics, the main challenges and trends of the national poultry market, which represents one of the most relevant agricultural activities due to its contribution to food security, rural employment and the supply of animal protein. Based on statistical data, institutional records and the collection of primary information through a questionnaire aimed at key actors in the sector, critical aspects related to the application of accounting standards in the management of biological assets are evidenced, as well as structural gaps that affect the efficiency and sustainability of the sector.

Relevant accounting and financial information has been identified in several provinces of Ecuador, which allows contextualizing the behavior of the poultry sector in the territories where this activity represents a significant part of the productive apparatus. Among these provinces, Tungurahua, Cotopaxi and Guayas stand out, which concentrate the largest number of active business registrations, as well as the highest values in terms of total assets, local net sales (0% VAT) and profit for the year, key variables to evaluate the financial and accounting dimension of the sector (Table 1).

These data constitute a fundamental basis for financial analysis, since they allow the performance of poultry production units to be compared from an accounting perspective, especially with regard to the application of international regulations such as IAS 41 on Agriculture, which regulates the treatment of biological assets. Within this group of provinces, Tungurahua stands out for registering the highest percentages in the variables analyzed, which shows its leadership and relevance within the national poultry activity (Table 1). Therefore, deepening the study of this province is strategic, since knowing the reality of a highly representative region allows generating more solid and generalizable conclusions about the current state and challenges in the application of accounting standards in the Ecuadorian poultry sector.

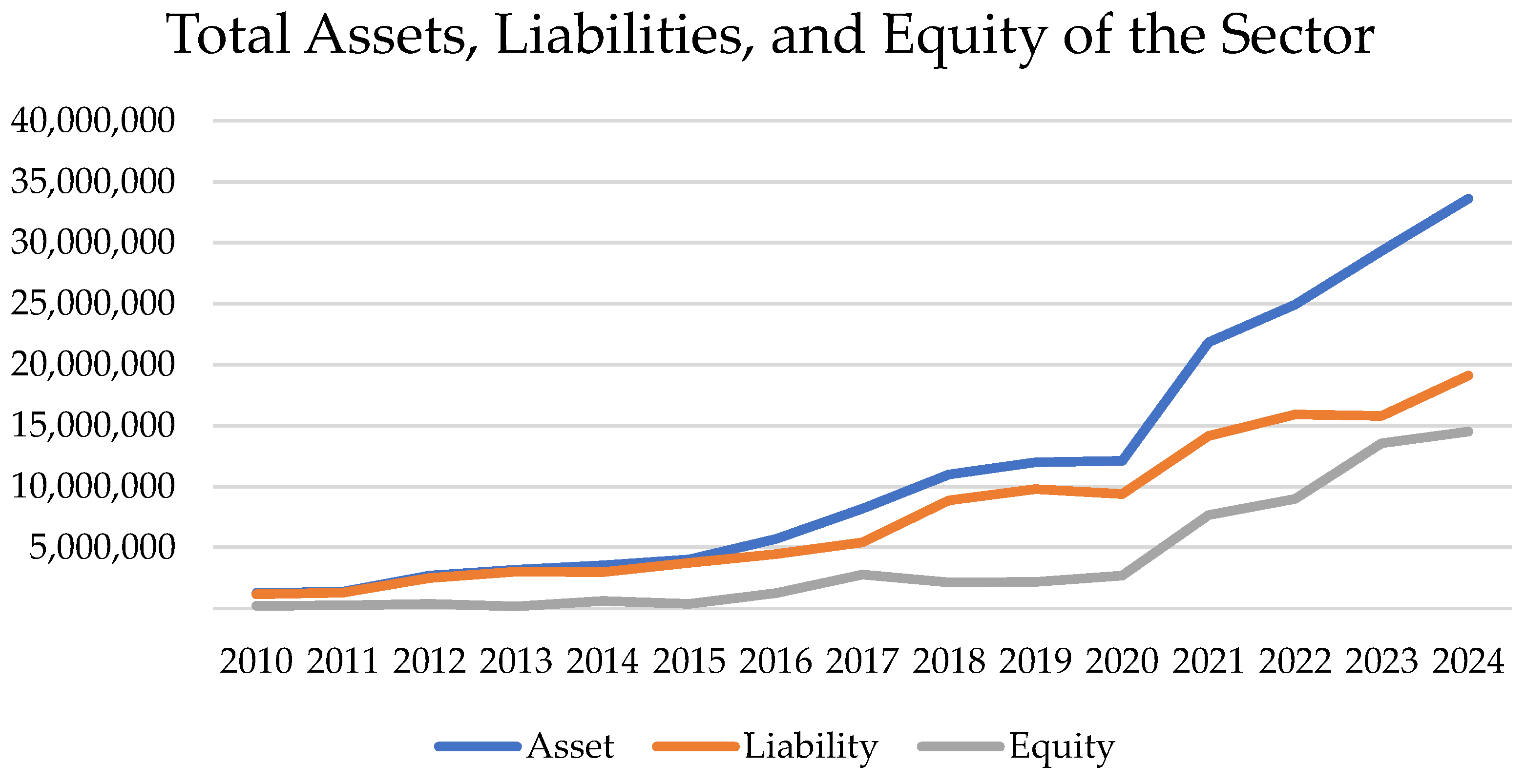

Figure 1 shows the evolution of the assets, liabilities and equity of the poultry sector in the province of Tungurahua between 2010 and 2024, with sustained and significant growth in the three financial components. Total assets show a constant increase, exceeding 30 million in 2024, which reflects an expansion in investment and acquisition of productive resources within the sector, including biological assets, such as growing birds, laying hens and other elements linked to the poultry cycle. This increase can be interpreted as an indicator that companies are strengthening their productive structure and improving their accounting systems to properly record such assets in accordance with IAS 41.

Liabilities also show parallel growth, suggesting higher financial leverage that could be earmarked for technological upgrading or the acquisition of high-value biological assets. However, equity continues to rise, indicating that companies are not only increasing their debts, but are also generating equity value, increasing their stockholders' equity and improving their financial sustainability. This behavior is consistent with a more rigorous application of international accounting standards since a correct valuation of biological assets at fair value in this type of company allows the real economic value of the business to be reflected more accurately. In this context, Tungurahua's accounting information not only shows dynamism, but also allows us to infer a greater degree of maturity in the adoption of modern accounting practices in the poultry sector.

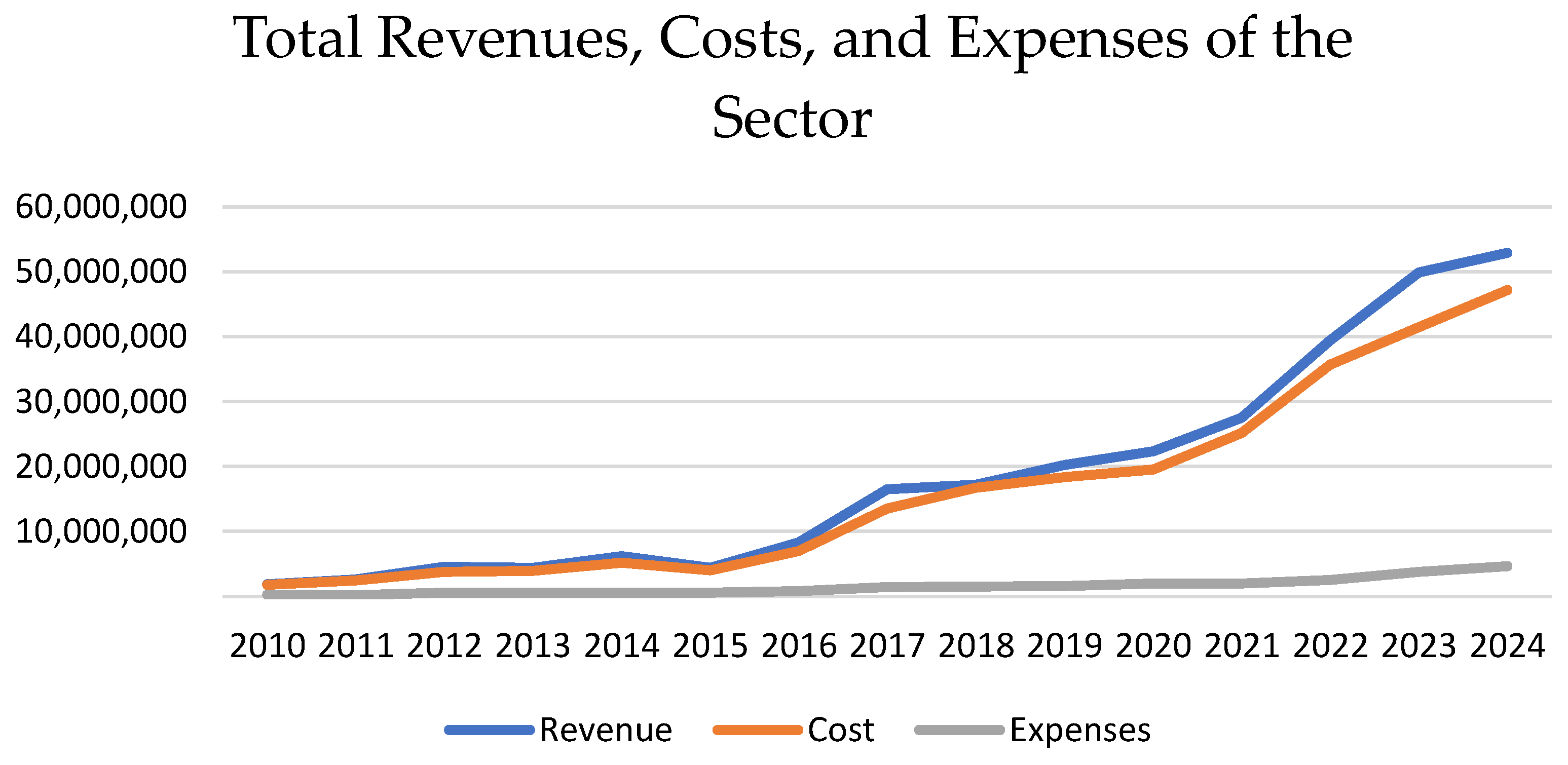

The analysis of the evolution of income, costs and expenditures of the poultry sector in the province of Tungurahua between 2010 and 2024 reflects a notable growth in the economic dynamics of the sector (Figure 2). Total revenues show a sustained upward trend, exceeding 55 million dollars in 2024, which indicates a significant increase in production and marketing, of products such as eggs. This pattern suggests efficient management of productive resources, where biological assets, when properly valued, have a direct impact on the calculation of the cost of sales and the correct determination of the result for the year.

Operating expenses, on the other hand, show more moderate growth, remaining significantly below revenues and costs, which reinforces the idea of an efficient business structure. In this context, the application of IAS 41 acquires a key role since it allows biological assets to be objectively valued at fair value minus the estimated costs at the point of sale. This accounting practice has a direct effect on the determination of income and costs, especially in a sector intensive in biological cycles such as poultry. Consequently, the behavior of these variables in Tungurahua shows not only a high level of productive activity, but also that it must take a growing accounting awareness about the importance of adequately reflecting the economic value of biological assets in the financial statements.

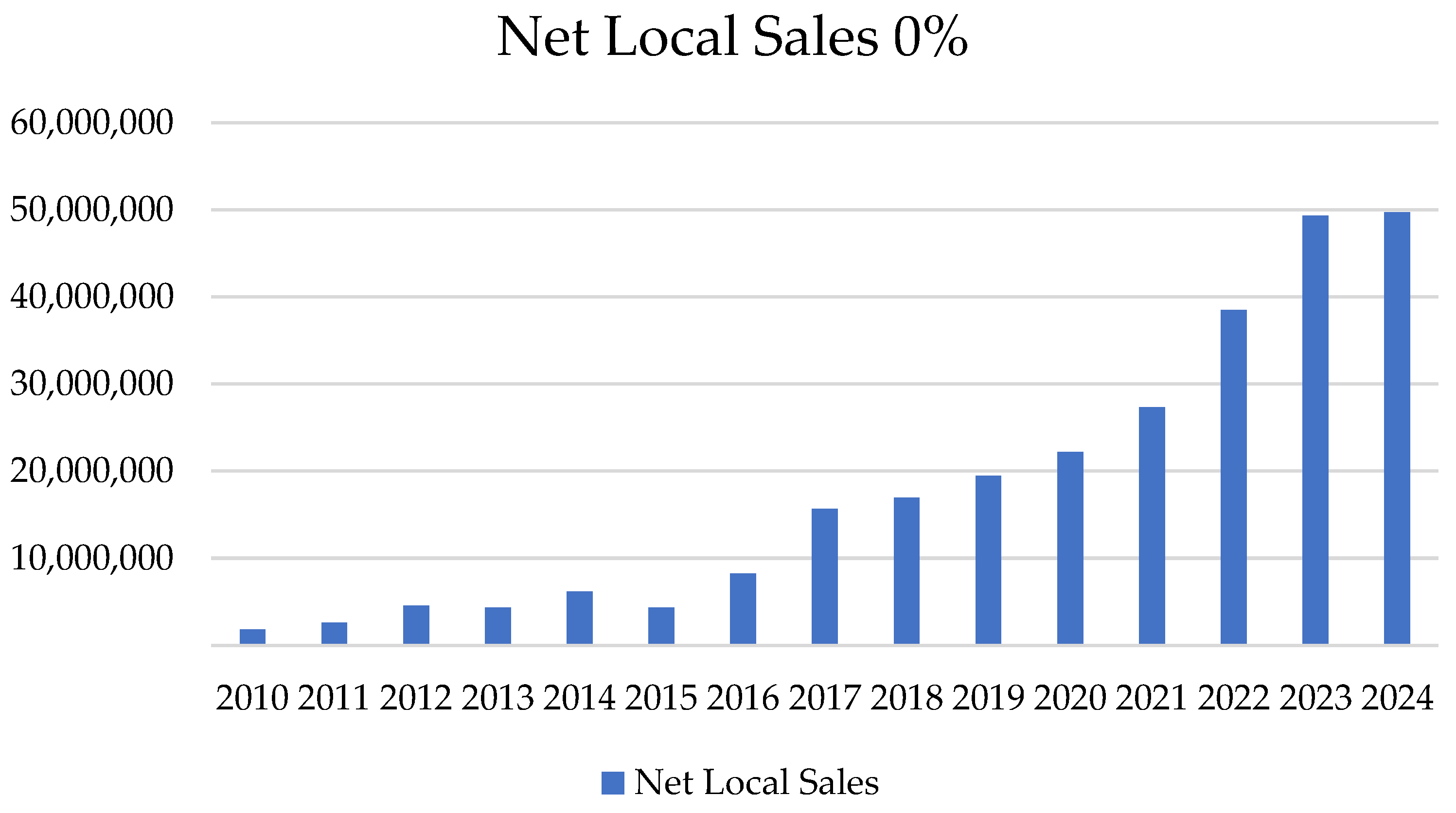

The following Figure 3 presents the evolution of net local sales taxed with 0% VAT from 2010 to 2024, reflecting sustained growth, especially from 2016 onwards. In 2022, 2023 and 2024, a stagnation in the maximum value is observed, exceeding 50 million, which denotes a stabilization of the market or production volume. The notable increase in net local sales indicates a steady expansion of the poultry sector in Tungurahua. This growth may be associated with increased demand for poultry products (eggs, chickens, by-products), reflecting their importance in the local economy. The fact that these are 0% of sales suggests that they are VAT-exempt products due to their essential or nutritional nature, as is often the case with unprocessed agricultural products. Such a significant increase in sales requires companies to conduct rigorous control and in accordance with accounting standards, such as IAS 41 - Agriculture, for the fair measurement of biological assets (growing birds, layers, etc.). This is crucial to accurately reflect the financial situation. The correct application of accounting standards allows poultry producers to correctly value their outstanding assets and project future revenues. This favors both internal decision-making and the trust of third parties (investors, financial institutions, regulators).

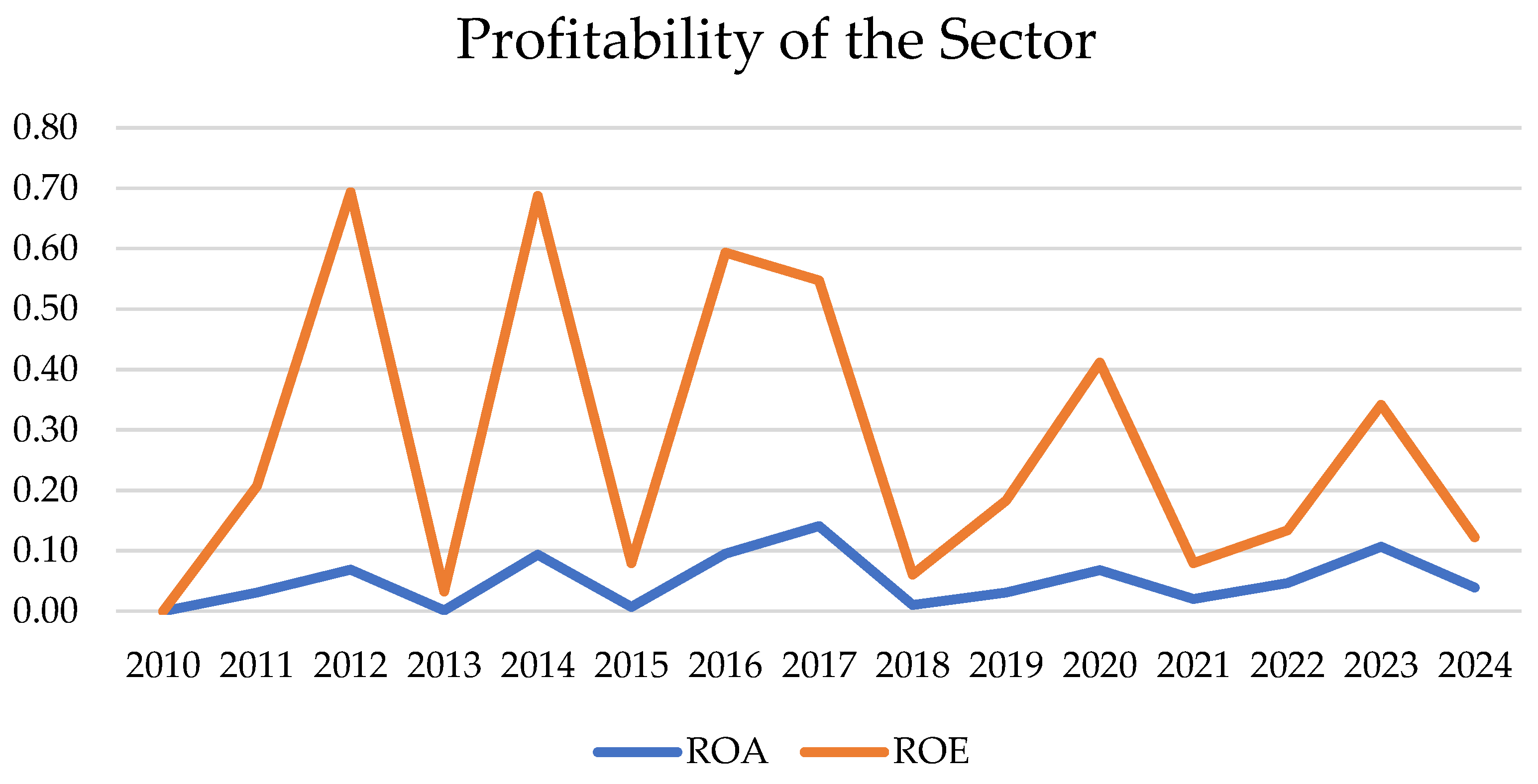

Figure 4 shows the evolution of the ROA (Return on Assets) and ROE (Return on Equity) of the poultry sector in Tungurahua between 2010 and 2024. The performance of ROA remains stable with slight variations, indicating that the sector has managed to use its assets efficiently in generating profits, although with modest margins. On the other hand, ROE is more volatile, with high peaks in certain years (2012, 2014, 2016) and subsequent abrupt falls, which reflects a high sensitivity of the return on equity to operational, financial or short-term factors of the economic environment.

This behavior suggests that, although poultry companies have maintained some control over the use of their assets, the capital structure and profitability for owners has been unstable. This could be associated with poor accounting practices or the lack of systematic application of standards such as IAS 41, which would allow a correct valuation of biological assets and, consequently, a more faithful presentation of financial results. In this context, implementing sound accounting standards would favor greater transparency and efficiency in management, improving confidence in the sector and facilitating strategic financial decisions based on verified and comparable information.

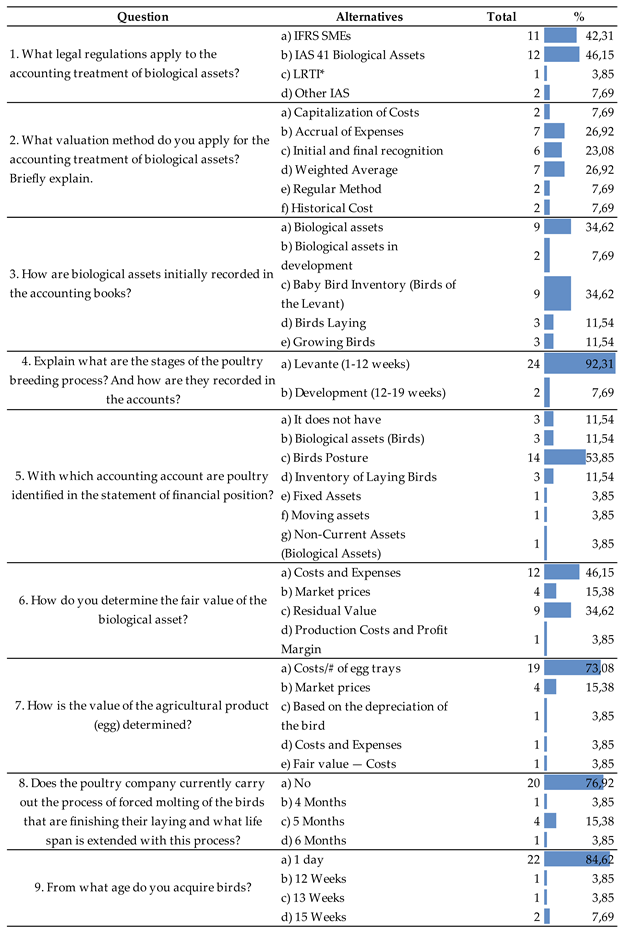

As part of this study, a questionnaire was applied to 26 representatives of poultry companies active in the province of Tungurahua, with the aim of knowing their perception regarding the application of accounting standards in the valuation of biological assets and their influence on business decision-making. The results show that a significant majority of respondents recognize the importance of reflecting the real value of biological assets (such as growing birds and layers) in financial statements, especially to obtain useful, timely and transparent information (Table 2).

Limitations in the practical implementation of IAS 41 were identified, related to lack of technical knowledge, lack of trained personnel and the absence of clear valuation methodologies. Despite this, the representatives pointed out that having financial information adjusted to the fair value of biological assets significantly improves planning, cost control and profitability evaluation, which shows that there is a positive assessment of their usefulness for business management, although challenges still persist in their proper accounting application.

Table 3 presents a summary of the most important results of the information acquired by the representatives of the companies engaged in the poultry sector, especially in egg production. This reflects their analysis and interpretation to know the broad and real panorama of the valuation of biological assets.

The general analysis of the results of the questionnaire applied to the representatives of 26 poultry companies in the province of Tungurahua reveals a broad panorama in terms of the level of knowledge and accounting application of biological assets. Although a significant part of the respondents recognize the IAS 41 standard as regulating the accounting treatment of these assets and state that they apply practices related to their valuation, there are still inconsistencies and diversity of criteria in key aspects such as valuation methods, accounting classification and initial registration. Most companies identify laying birds as relevant assets and use practical methods such as cost per tray to value production, reflecting an operational rather than a technical approach. Likewise, there is evidence of a limited application of fair value, in contrast to what is required by international regulations, and a tendency not to apply biological optimization processes such as forced molting. These results indicate that, although there is an accounting knowledge base, greater technical training and standardization of practices are required to achieve a more accurate and uniform implementation of IAS 41, which would result in more reliable financial information for individual and sectoral decision-making, knowing that geographical location and the homogenization of activities are considered.

In order to complement the quantitative analysis of the results of the questionnaire applied to the representatives of the poultry sector in the province of Tungurahua, a diagram of the concurrence of keywords was used. This methodological resource allows us to visualize the most frequent semantic relationships between relevant concepts extracted from the analysis and interpretation of the answers (Figure 5). By identifying the terms that appear together most regularly, the diagram contributes to uncovering thematic necessities, discursive trends, and conceptual patterns, facilitating a deeper understanding of how the accounting and regulatory aspects associated with the valuation of biological assets are perceived and implemented. This tool also makes it possible to verify the coherence between the declared results and the predominant concepts in the respondents' discourse.

The concurrence diagram shows that the terms "biological assets", "accounting", "valuation", "control", "IAS 41" and "cycle" occupy central positions, which confirms their high frequency and relevance in the conceptual analysis of the questionnaire. The strong association between peers such as "fair value – biological assets", "accounting control – biological cycle" and "cost – valuation" indicates that respondents link accounting management with the operational and productive management of birds. Likewise, the presence of terms such as "classification", "initial registration" and "inventory" reveals that there is concern for the adequate accounting treatment from the first phases of the production cycle. However, the predominance of concepts associated with the cost-over-fair value approach also reflects a gap between international regulations and their practical application. The dispersion of terms related to valuation methods and classification criteria reveals the heterogeneity of accounting approaches in the sector, which must be considered when interpreting the strength of the semantic connections in the graph. Another relevant aspect is that the diagram reflects the perceptions and language of the business representatives, therefore, its value lies more in showing how the topic is conceptualized in practice than in representing a formal regulatory structure. Overall, the diagram reinforces the idea that, although there is awareness of the importance of biological assets, there is still a need to move towards greater accounting standardization and technical alignment with the principles established by IAS 41.

5. Discussion

The present discussion is structured around the central question of the research: How are the accounting standards for the valuation of biological assets applied in companies in the poultry sector (ISIC A0146.03) of Tungurahua, and what is the perception of their owners regarding their impact on financial information and decision-making? This question seeks to integrate two fundamental dimensions: on the one hand, the technical application of IAS 41 – Agriculture in the recognition, measurement and presentation of biological assets; and on the other, the subjective assessment of business representatives on the usefulness of such information in the accounting and strategic management of their organizations. Through the analysis of the results obtained through the questionnaire, as well as the financial and documentary study of the sector, the empirical findings are contrasted with current regulations and with previous studies, in order to understand the degree of alignment between accounting theory and business practice in a highly productive and biologically intensive sector such as poultry.

5.1. Q1: Are the International Financial Reporting Standards (NIFF) Fully Applied in the Accounting Record of Biological Assets in Companies in the Poultry Sector in Tungurahua?

The results obtained allow us to affirm that the IFRS applied in a large percentage is IAS 41 in the poultry sector of Tungurahua, but this is not conducted in an integral or standardized way. Although a significant percentage of respondents (46.15%) recognize the existence and relevance of this international standard, in practice there is a diversity of valuation methods such as the IFRS SMEs (42.31%), the Internal Tax Regime Law (3.85%) and other types of IAS (7.69%), which do not necessarily respond to the central principle of IAS 41: the measurement at fair value less than the estimated costs at the point of sale. In addition, there is ambiguity in the initial registration of biological assets, since they are classified in some cases as inventories (34.62%) and in others as biological assets (42.31%), which generates accounting inconsistencies and limitations in the comparability of financial information.

The application of IAS 41 in the accounting of biological assets in agricultural enterprises has not been implemented uniformly across regions or among organizations themselves, evidencing a divergence in the interpretation and enforcement of international standards (Bohušová & Svoboda, 2017; Pires et al., 2021; Silva et al., 2020). Various studies agree that, although IAS 41 is the main standard used for the recognition, measurement and disclosure of biological assets, its practical implementation has limitations (Bozzolan et al., 2016; Herrera et al., 2021; Menezes & Ciampaglia, 2023; Ríos et al., 2024). For example, in the Czech Republic, a significant gap has been identified between the accounting regulatory framework and the way biological assets are recorded in practice, especially in relation to biological transformation and information disclosure (Jana & Marta, 2014; Sedláček, 2014). Similarly, a study conducted in Vietnam explored the relationship between the correct application of accounting standards and the profitability of agricultural enterprises, concluding that the effective adoption of international standards requires not only a legal framework, but also continuous training of human resources and the incorporation of technological tools (Hoa et al., 2022).

5.2. Q2: What Level of Technical Knowledge do the Owners or Accountants Have About IAS 41 and How Does it Influence Its Practical Application?

The findings of the study show that, although a significant part of the surveyed business representatives claim to be aware of IAS 41, this knowledge is superficial and, in many cases, limited to a general understanding of the concept of biological assets, without a clear mastery of its technical and methodological implications. This situation is reflected in the variety of accounting criteria used for the registration and identification of birds as biological assets (11.54%), laying birds (53.85%), poultry inventory (11.54%), fixed assets (3.85%), non-current assets (3.85%) and non-owners (11.54%). On the other hand, valuation is different, such as cost capitalization (7.69%), accumulation of expenses (26.92%), initial and final recognition (23.08%), weighted average (26.92%), regular method (7.69%) and historical cost (7.69%), as well as in the preference for practical methods such as unit cost per tray, which are useful for operational control, but do not comply with regulatory requirements on measurement at fair value. The lack of specialized training and the absence of accounting professionals with experience in international standards have a direct influence on the partial application of IAS 41, which has an impact on the reliability and transparency of financial reporting (Mirović et al., 2019). In this sense, the current level of technical knowledge limits the correct implementation of regulations and, consequently, restricts the strategic use of financial statements as a tool for decision-making based on objective and normatively supported information (Middelberg et al., 2012; Peštović et al., 2022).

Although IAS 41 has the potential to improve the quality and transparency of accounting information, its application may also introduce variability in the methods used and subjectivity in estimates, which affects the comparability and relevance of financial statements between different entities (Altarawneh, 2023; Giertliová et al., 2017). The measurement of fair value, the central axis of the standard, requires a high level of technical knowledge and methodological mastery, such as the use of discounted cash flow techniques or specific valuation models (Xie et al., 2020).

Various studies agree that one of the main obstacles to its correct implementation is the lack of specialized training in agricultural and international accounting (Bozzolan et al., 2016; Fernandes et al., 2016; Wen-hsin Hsu et al., 2019). This lack generates an inconsistent application of the standard, which not only responds to differences in the accounting policy of each entity, but also to gaps in professional training. Therefore, it is essential that both owners and accounting managers receive continuous and specialized training, which allows them to understand and properly apply the principles and requirements of IAS 41 in current contexts.

5.3. Q3: How Does the Lack of Homogenization Affect the Application of Accounting Standards on the Presentation and Comparability of Financial Statements in Companies in the Poultry Sector (ISIC A0146.03) of Tungurahua?

The quantitative results of the study show a lack of homogenization in the accounting criteria applied by the companies in the poultry sector of Tungurahua, which directly affects the presentation and comparability of the financial statements. For example, when asked about the method used to value agricultural products, the answers were divided between the method of cost per bucket of eggs (73.08%), market prices (15.38%), based on the amortization of the bird (3.85%), costs and expenses (3.85%) and fair value less costs (3.85%), which shows divergent criteria for the same accounting treatment. In addition, in terms of determining the fair value of the biological asset, there are costs and expenses (46.15%), market prices (15.38%), residual value (34.62) and production costs and profit margin (3.85%), reflecting an inconsistency in the accounting valuation.

This diversity of practices reveals that the absence of common guidance or the limited technical implementation of IAS 41 generates financial statements that are not comparable between companies, this compromises the reliability of sectoral analyses and makes it difficult for investors, regulators or administrators to make informed decisions (Solovyov & Kuznetsov, 2011). Therefore, the data suggest that the homogenization of accounting criteria and the correct application of regulations are necessary conditions to improve the quality and usefulness of financial information (Pavić, 2020; Solovyov & Kuznetsov, 2011).

In addition, problems arising from continuous changes in IFRS are identified, which can compromise the application of fundamental principles such as consistency and comparability. This situation makes it difficult both to compare financial statements over time and between different companies in the sector (Felski, 2017; Smith et al., 2021). The flexibility inherent in IFRS in terms of asset recognition, measurement and disclosure, while it seeks adaptability, also leads to disparities in accounting practices (Altarawneh, 2023), especially in sectors with particular biological and productive characteristics, such as the poultry industry. These variations are influenced not only by the specific nature of the sector, but also by regional accounting practices and varying levels of technical knowledge (Mirović et al., 2019). Faced with this scenario, it is necessary to move towards the standardization of accounting criteria, the reduction of excessive interpretative margins, as well as strengthening supervision by regulatory bodies and promoting technological integration (Mirović et al., 2019; Peštović et al., 2022; Sakovié et al., 2020). The lack of homogenization generates significant barriers, such as information asymmetries, inconsistencies in financial reporting, and difficulties in objectively assessing economic performance among comparable entities (S. R. Ika et al., 2022; Wen-hsin Hsu et al., 2019).

Studies have shown that the adoption of IAS and IFRS contributes to higher accounting quality, reduced discretionary management of results and more timely recognition of losses, thereby strengthening the transparency of financial statements (Bohušová & Svoboda, 2017; S. Ika et al., 2024). In particular, companies that implement IAS 41 consistently and sustainably over time tend to present more accurate and reliable information about their biological assets, which is often associated with larger organizations, greater profitability and financial strength. This rigorous application reflects a commitment to accounting transparency and facilitates informed decision-making both internally and externally (Sedláček, 2014; Solovyov & Kuznetsov, 2011). Likewise, companies with a high intensity of biological assets tend to be more committed to their adequate disclosure, which not only improves the quality of financial information, but can also have a positive impact on market perception, access to financing, and long-term profitability (Felski, 2017; Middelberg et al., 2012; Wen-hsin Hsu et al., 2019).

6. Conclusions

6.1. Conclusions of the Study

This study analyzed the application of International Financial Reporting Standards (IFRS), with emphasis on IAS 41 – Agriculture, in companies in the poultry sector in the province of Tungurahua, Ecuador, specifically those registered under ISIC code A0146.03 for poultry egg production. From a mixed approach that included the analysis of financial data, descriptive statistics and the perception of business representatives, it was possible to obtain a comprehensive view of the degree of regulatory compliance, the technical knowledge of accounting managers and the effects that the lack of accounting homogenization generates on the quality of financial statements.

Regarding the first research question, the results show that IAS 41 is not fully applied in the companies in the poultry sector analyzed. Although a significant part of the respondents claim to be aware of the standard and follow some of its guidelines, in practice a partial adoption is observed, influenced by the preference for alternative valuation methods such as unit cost per tray or accrued cost. These approaches are not always aligned with the fair value principle, as required by IAS 41, resulting in a significant gap between what the standard establishes and what is actually implemented in the local business context.

In relation to the second research question, it was found that the level of technical knowledge about IAS 41 among owners and accounting managers is limited and heterogeneous. Although there is awareness of the existence of the norm, its technical understanding is superficial, which translates into an inadequate or confusing execution of normative procedures. The absence of specialized training in agricultural and international accounting, coupled with the lack of external professional advice, limits the ability of companies to properly implement the criteria for the recognition, measurement and disclosure of biological assets.

Regarding the third research question, the lack of homogenization in the accounting application generates serious consequences for the presentation and comparability of financial statements. The different practices used in asset classification (such as inventory, birds in laying or others) and the measurement methods adopted lead to inconsistent accounting reporting, which hinders both cross-company benchmarking and decision-making based on standardized information. This dispersion also reflects the absence of clear sectoral guidelines and the urgent need for regulatory oversight.

The findings also confirm that companies with higher bio-asset intensity, and with a more rigorous adoption of IAS 41, tend to exhibit more complete, transparent and useful financial statements, suggesting a direct relationship between regulatory commitment and the quality of financial reporting. In addition, it is highlighted that the proper application of these standards not only improves internal accounting, but can also contribute to the profitability, sustainability and competitiveness of the poultry sector, by facilitating access to financing and improving the perception of risk by third parties.

Finally, it is concluded that in order to achieve an effective implementation of IAS 41 in the poultry sector of Tungurahua, it is essential to strengthen accounting training processes, promote the homogenization of sectoral accounting criteria and establish technical and regulatory supervision mechanisms that guide companies towards a coherent and systematic application. The improvement in these aspects will allow the generation of more reliable, comparable and useful financial information for strategic management, auditing, performance evaluation and decision-making at the business and regulatory level.

6.2. Future Lines of Research

Based on the findings obtained, a relevant future line of research is to explore the financial and operational impact of fully applying IAS 41 in companies in the agricultural sector, including not only poultry, but also activities such as livestock, fruit production or transient crops. This research could incorporate econometric models or longitudinal case studies to analyze how the full adoption of the standard affects key variables such as profitability, operational efficiency, access to credit or the market value of companies, thus allowing a more robust evaluation of the cost-benefit of its implementation.

Another valuable line of research would be the development of specific sectoral accounting guidelines for biological assets in emerging economies, considering the reality of agricultural micro, small and medium-sized enterprises (MSMEs). This approach would make it possible to propose simplified but normatively aligned criteria, which facilitate the practical application of IAS 41, especially in regions with a low level of digitalization, limited technical training and little supervision. In addition, the analysis of the role of digital technologies and automated accounting systems could be incorporated as tools to close knowledge gaps and promote accounting standardization in the agricultural sector.

Author Contributions

Conceptualization, methodology, software, validation, formal analysis, investigation, resources, data curation and writing—original draft preparation, P.C.-Ll., M.A.-P., C.T.-M and C.B.-C.; writing—review and editing, visualization, supervision, project administration, P.C. Ll. All authors have read and agreed to the published version of the manuscript.

Institutional Review Board Statement

Not applicable.

Informed Consent Statement

Not applicable.

Data Availability Statement

The data used in this study come from official institutional sources in Ecuador, which are publicly available, as well as from a survey conducted specifically with representatives of the poultry sector in the province of Tungurahua. The survey data were collected for academic purposes and are available upon reasonable request to the corresponding author, in accordance with participant confidentiality and applicable ethical standards. Institutional information can be accessed through the relevant government portals.

Acknowledgments

The authors would like to express their gratitude to the Dirección de Investigación y De sarrollo (DIDE) of the Universidad Técnica de Ambato (UTA) for their support in the publication of this article, which stems from the research project entitled “Valuation of Biological Assets and the Reasonableness of Financial Information in the Poultry Sector, Egg Production, Tungurahua Prov ince”, under Code: SFFCAUD04, approved by Resolution No. UTA-CONIN-2023-0086-R issued by the Dirección de Investigación y Desarrollo (DIDE) of the Universidad Técnica de Ambato, Ecuador. All related investigations have provided additional data that complement the findings pre sented herein.

Conflicts of interest

The authors declare that they have no conflicts of interest.

References

- ACCA Global. (2024). IAS 41, Agriculture. https://www.accaglobal.com/gb/en/student/exam-support-resources/dipifr-study-resources/technical-articles/ias-41.

- Altarawneh, M. (2023). How Company Characteristics Influence Measurement Practices and Disclosure Level Prescribed within IAS 41. Journal of Risk and Financial Management, 16(6), 288. [CrossRef]

- Arimany, N. , Farreras, M. À., & Rabaseda, J. (2013). Alejados de la NIC 41: ¿Es correcta la valoración del patrimonio neto de las empresas agrarias? Economía Agraria y Recursos Naturales - Agricultural and Resource Economics, 13(1). [CrossRef]

- Bangsheng, X. , Meijuan, L., Randhir, T., Yi, Y., & Hu, X. (2020). Is the biological assets measured by historical cost value-related? Custos e Agronegócio, 16(1). http://www.custoseagronegocioonline.com.br/numero1v16/OK%206%20assets.

- Biljon, M. van, & Wingard, C. (2020). An agricultural sector assessment of biological asset valuation challenges with inputs considered from valuers. International Journal of Financial, Accounting, and Management, 2(3). [CrossRef]

- Biondi, Y. , & Oulasvirta, L. (2023). Accounting for Public Sector Assets: Comparing Historical Cost and Current Value Models. En Measurement in Public Sector Financial Reporting: Theoretical Basis and Empirical Evidence, 39-62. Emerald Publishing Limited. [CrossRef]

- Bohušová, H. , & Svoboda, P. (2017). Will the amendments to the IAS 16 and IAS 41 influence the value of biological assets? Agricultural Economics, 63(2), 53–64. [CrossRef]

- Bolzani, D. (2020). Thirty Years of Studies on Migrant Entrepreneurship: New Opportunities for Management Scholars. En Migrant Entrepreneurship,11-54. Emerald Publishing Limited. [CrossRef]

- Bozzolan, S. , Laghi, E., & Mattei, M. (2016). Amendments to the IAS 41 and IAS 16 - implications for accounting of bearer plants. Agricultural Economics (Zemědělská Ekonomika), 62(4), 160–166. [CrossRef]

- Carrión, K. , Caiminagua, M., & Soto, C. (2021). Tratamiento contable del Activo Biológico: Planta Productora, Enmienda a NIC 41. 593 Digital Publisher CEIT, 6(3). [CrossRef]

- CFN. (2024). Ficha Sectorial Aves de Corral. https://www.cfn.fin.ec/wp-content/uploads/2024/05/Ficha-Sectorial-Aves-de-corral.

- Chávez, R. B. , Chamba, L. A., Tobar, G. N., Jima, V. V., & Cortez, S. K. (2023). Aplicaciones y beneficios tributarios de la NIC 41 del sector agrícola de Ayapamba 2022. Ciencia Latina Revista Científica Multidisciplinar, 7(1). [CrossRef]

- CONAVE. (2021). El sector avícola es un dinamizador de la economía nacional. https://conave.

- Felski, E. (2017). How Does Local Adoption of IFRS for Those Countries That Modified IFRS by Design, Impair Comparability with Countries That Have Not Adapted IFRS? Journal of International Accounting Research, 16(3), 59–90. [CrossRef]

- Fernandes, E. , Fernandes, F., & Gonzaga, T. (2016). Biological Assets Mensuration and IAS 41 observance in South America. Custos e Agronegócio, 12(2), 333–351. http://www.custoseagronegocioonline.com.br/numero2v12/OK%2016%20biologicos%20english.

- Giertliová, B. , Dobšinská, Z., & Šulek, R. (2017). Comparison of the forest accounting system in Slovakia and IAS 41. Austrian Journal of Forest Science, 1–22. https://www.forestscience.at/content/dam/holz/forest-science/2017/heft1a/CB1701A_Article01.

- Guidolin, M. (2011). Markov Switching in Portfolio Choice and Asset Pricing Models: A Survey. Missing Data Methods: Time-Series Methods and Applications,2, 87-178). Emerald Group Publishing Limited. [CrossRef]

- Hadiyanto, A. , Puspitasari, E. K. ( 60(6), 1401–1411. [CrossRef]

- Herrera, A. , Herrera, A., & Chávez, G. (2021). NIC 41 y su incidencia en el precio por caja de banano ecuatoriano, período 2019-2020. Universidad y Sociedad, 13(3), 100–109. https://rus.ucf.edu.cu/index. 2079. [Google Scholar]

- Hinke, S. (2014). The Fair Value Model for the Measurement of Biological Assets and Agricultural Produce in the Czech Republic. Procedia Economics and Finance, 12, 213-220. [CrossRef]

- Hoa, N. , Duyen, N., Huyen, V., Quang, H., Huong, N., Tu, N., & Nguyet, B. (2022). Impact of Trained Human Resources, Adoption of Technology and International Standards on the Improvement of Accounting and Auditing Activities in the Agricultural Sector in Vietnam. AgBioForum, 24(1), 59–71. https://agbioforum.org/menuscript/index.

- IAS. (2022). International Accounting Standard IAS 41. IAS 41 BC. https://aasb.gov.au/admin/file/content105/c9/IAS41_BC_1-22.

- Ifeanyieze, F. O. , Asogwa, C. I., Nwankwo, C. U., Ekenta, L. U., Ezebuiro, F. N., Eze, G. E., Onu, F. M., Onah, F. C., Asogwa, V. C., Isiwu, E. C., & Nwangbo, A. F. (2021). Effect of poultry absorptive capacity on the farms’ economic and commercial performance. Journal of Agribusiness in Developing and Emerging Economies, 13(1), 119-140. [CrossRef]

- Ika, S. R. , Susetyo, R., Pribadi, A., Dwiwinarno, T., & Widagdo, A. K. (2022). Factors influencing biological asset disclosures in agricultural companies in Indonesia. IOP Conference Series: Earth and Environmental Science, 1114(1), 012074. [CrossRef]

- Ika, S. , Farida, F., Asih, S., Okfitasari, A., & Widagdo, A. (2024). The impact of biological asset disclosures and economic sustainability on firm value: Evidence from agricultural companies in Indonesia. IOP Conference Series: Earth and Environmental Science, 1297(1), 012069. [CrossRef]

- INEC. (2020). Sector Avícola Ecuador. https://obest.uta.edu.ec/wp-content/uploads/2020/09/Sector-avicola-Ecuador.

- Jana, H. , & Marta, S. (2014). The Fair Value Model for the Measurement of Biological Assets and Agricultural Produce in the Czech Republic. Procedia Economics and Finance, 12, 213–220. [CrossRef]

- Kurniawan, R. , Mulawarman, A. D., & Kamayanti, A. (2014). Biological Assets Valuation Reconstruction: A Critical Study of IAS 41 on Agricultural Accounting in Indonesian Farmers. Procedia - Social and Behavioral Sciences, 164, 68-75. [CrossRef]

- Majercakova, D. , & Skoda, M. (2015). Fair value in financial statements after financial crisis. Journal of Applied Accounting Research, 16(3), 312-332. [CrossRef]

- Menezes daSilva, R. L. , Nardi, P. C. C., & Ribeiro, M. de S. (2015). Earnings Management and Valuation of Biological Assets. Brazilian Business Review, 12(4), 1-26. [CrossRef]

- Menezes, R. , & Ciampaglia, P. (2023). IAS 41 and biological assets in Brazil. Revista Catarinense Da Ciência Contábil, 22, e3365. [CrossRef]

- Menglikulov, B. Y. , Davletov, I. R., & Yusupova, M. B. (2024). Improvement of Organizational and Methodological Aspects of Identification and Accounting of Biological Assets in Livestock Based on International Standards. En Development of International Entrepreneurship Based on Corporate Accounting and Reporting According to IFRS, 33, 31-38. Emerald Publishing Limited. [CrossRef]

- Middelberg, S. L. , Buys, P. W., & Styger, P. (2012). The accountancy implications of commodity derivatives: A South African agricultural sector case study. Agrekon, 51(3), 97–116. [CrossRef]

- Mirović, V. , Milenković, N., Jakšić, D., Mijié, K., Andrašić, J., & Kalaš, B. (2019). Quality of biological assets disclosures of agricultural companies according to international accounting regulations. Custos e Agronegócio, 15(4), 43–58. http://www.custoseagronegocioonline.com.br/numero4v15/OK%203%20disclosure%20english.

- Nakasone, G. T. , & Castillo, C. (2023). Implementation of IAS 41 (Agriculture): The case of a Peruvian SME. Contabilidad y Negocios, 18(35), 14-38. [CrossRef]

- Ning, D. , Irfan-Ullah, Majeed, M. A., & Zeb, A. (2022). Board diversity and financial statement comparability: Evidence from China. Eurasian Business Review, 12(4), 743-801. [CrossRef]

- Nuhu, N. A. , Baird, K., & Su, S. (2021). The Impact of Environmental Activity Management and Sustainability Strategy on Triple Bottom Line Performance. En Advances in Management Accounting, 33, 175-207. Emerald Publishing Limited. [CrossRef]

- Nurunnabi, M. (2021). The Economic Impact of International Financial Reporting Standards (IFRS) Implementation, Emerald Insight. https://emerald.pucp.elogim.com/insight/content/doi/10. 1108. [Google Scholar]

- Osipchuk, D. , Chyzhevska, L., Petryshyn, L., Pryimak, S., Loboda, N., & Antoshchenkova, V. (2024). Accounting for government grants in agricultural enterprises’ reporting according to IFRS. Financial and Credit Activity: Problems of Theory and Practice, 4(57), 143-154. Scopus. [CrossRef]

- Pavić, I. (2020). Analiza učinaka promjena u Međunarodnim standardima financijskoga izvještavanja na usporedivost i dosljednost financijskih izvještaja. Ekonomski Pregled, 71(4), 331–358. [CrossRef]

- Peštović, K. , Medved, I., Rađo, D., Jakšić, D., & Saković, D. (2022). The impact of accounting regulation basis to the mandatory biological assets reporting: evidence from the Serbian agricultural production companies. Custos e Agronegócio, 18(3), 94–109. http://www.custoseagronegocioonline.com.br/numero3v18/OK%206%20biological.

- Pires, A. , Lemos, S., & Lemos, D. (2021). Assessment of Biological Assets in Agribusiness. Custos e Agronegócio, 17(3), 85–107. http://www.custoseagronegocioonline.com.br/numero3v17/OK%205%20biological.

- Poljašević, J. , Vašiček, V., & Jovanović, T. (2019). Comparative review of dual reporting in public sector in three south-east European countries. Journal of Public Budgeting, Accounting & Financial Management, 31(3), 325-344. [CrossRef]

- Ríos, K. , Carvajal, H., Prado, E., & Espinoza, M. (2024). Activos biológicos de una camaronera: NIC 41 y su aplicación en el ámbito contable tributario. Multidisciplinary Latin American Journal (MLAJ), 2(2), 107–123. [CrossRef]

- Rodrigues, V. D. V. , Wander, A. E., & Rosa, F. S. da. (2025). Poultry Eco-Controls: Performance and Accounting. Agriculture, 15(12), Article 12. [CrossRef]

- Sakovié, D. , Peštović, K., Tica, T., & Rado, D. (2020). The impact of quality of biological assets and properties disclosures on agricultural company`s performance. Custos e Agronegócio, 20(1), 91–110. http://www.custoseagronegocioonline.com.br/numero1v20/OK%205%20assets.

- Sedláček, J. (2014). Harmonisation of agricultural accounting. Acta Universitatis Agriculturae et Silviculturae Mendelianae Brunensis, 55(6), 149–156. [CrossRef]

- Silva, A. , Costa da Silva, D., Souza, A., & Marcos, E. (2020). Analysis of compliance level of biological assets in public companies. Custos e Agronegócio, 16(1), 222–250. http://www.custoseagronegocioonline.com.br/numero1v16/OK%2010%20conformidade%20english.

- Silva, P. D. , Gunarathne, N., Kumar, S. (2024). Exploring the impact of digital knowledge, integration and performance on sustainable accounting, reporting and assurance. Meditari Accountancy Research, 33(2), 497-552. [CrossRef]

- Smith, C. , Venter, E., & Stiglingh, M. (2021). Substance and Form Adoption of International Financial Reporting Standards and Financial Statement Comparability: Evidence from South Africa. The International Journal of Accounting, 56(04). [CrossRef]

- Solovyov, A. , & Kuznetsov, I. (2011). International accounting in the 21st century. New York : Nova Science Publishers. https://emu.tind.io/record/625840.

- Valverde, V. , Gavilanes, I., Idrovo, J., Carrera, L., Buri, S., Salazar, K., & Paredes, C. (2022). Characterization of Agro-Livestock Wastes for Composting in Rural Zones in Ecuador: The Case of the Parish of San Andrés. Agronomy, 12(10), Article 10. [CrossRef]

- Wang, C.-N. , Nguyen, V. T., Kao, J.-C., Chen, C.-C., & Nguyen, V. T. (2021). Multi-Criteria Decision-Making Methods in Fuzzy Decision Problems: A Case Study in the Frozen Shrimp Industry. Symmetry, 13(3), Article 3. [CrossRef]

- Watkiss, P. (2019). Decision-making and economics of adaptation to climate change in the fisheries and aquaculture sector. Food and Agriculture Organization of the United Nations. https://openknowledge.fao.org/server/api/core/bitstreams/32239839-8f34-4bd8-8a8bebba5c1dceeb/content.

- Wen-hsin Hsu, A. , Liu, S., Sami, H., & Wan, T. (2019). IAS 41 and stock price informativeness. Asia-Pacific Journal of Accounting & Economics, 26(1–2), 64–89. [CrossRef]

- Wudhikarn, R. , Anantana, T., Phongthiya, T., Paphawasit, B., & Pattanasak, P. (2025). Developing an intellectual capital benchmarking approach of business incubators. Journal of Intellectual Capital, 26(3), 616-643. [CrossRef]

- Xie, B. , Liu, M., Randhir, T., Yi, Y., & Hu, X. (2020). Is the biological assets measured by historical cost value-related? Custos e Agronegócio, 16(1), 122–150. http://www.custoseagronegocioonline.com.br/numero1v16/OK%206%20assets.

Figure 1.

Evolution of the total assets, liabilities and equity of the sector.

Figure 2.

Evolution of total income, costs and expenses of the sector.

Figure 3.

Evolution of net local sales with 0% VAT in the sector.

Figure 4.

Evolution of ROA and ROE profitability in the sector.

Figure 5.

Concurrency diagram.

Table 1.

Economic activity in different provinces of Ecuador.

| Province | Total Assets | % | Profit of the exercise | % | Local net sales 0% | % |

|---|---|---|---|---|---|---|

| Chimborazo | 614.679 | ,94 | 74.076 | 3,30 | 3.147.819 | 4,86 |

| Cotopaxi | 17.442.399 | 26,81 | 133.983 | 5,96 | 2.960.329 | 4,57 |

| Gold | 1.440.412 | 2,21 | 74.615 | 3,32 | 3.909.594 | 6,04 |

| Guayas | 8.542.466 | 13,13 | 76.965 | 3,42 | 46.571 | ,07 |

| Manabí | 1.482.137 | 2,28 | - | - | 204.962 | ,32 |

| Pichincha | 1.916.002 | 2,95 | 114.027 | 5,07 | 4.728.077 | 7,31 |

| Tungurahua | 33.617.708 | 51,68 | 1.774.363 | 78,93 | 49.710.426 | 76,82 |

| Total | 65.055.803 | 100 | 2.248.028 | 100 | 64.707.777 | 100 |

Table 2.

Results of the questionnaire applied to representatives of companies in the sector.

|

*Ecuadorian Tax Regime Law.

Table 3.

Analysis of the relevant results of the questionnaire.

| Question | Relevant Result | Analysis and Interpretation |

|---|---|---|

| 1. What accounting regulations apply to the treatment of biological assets? | IAS 41 (46.15%) | There is evidence of a majority knowledge of the international standard that regulates biological assets, which is positive for technical and accounting adoption in the sector. |

| 2. What valuation method applies to biological assets? | Accrued expense and weighted method (26.92% each) | There is no single dominant method, which reflects heterogeneity in the accounting criteria used, which may affect the comparability of financial statements. |

| 3. How are biological assets initially registered? | Inventory of baby/biological birds (34.62% each) | There is a tendency to record assets as inventory or as biological assets, indicating some ambiguity in the initial categorization, due to a lack of clear guidelines. |

| 4. Stages of the poultry production process | Lift (1–12 weeks): 92.31% | There is clarity about the initial phases of the biological cycle, which contributes to an orderly record from early stages of production. |

| 5. Which accounting account is identified with birds in the financial statements? | Birds in lying (53.85%) | Most recognize laying birds as relevant assets, but accounting classification needs to be improved to correctly reflect their biological nature. |

| 6. How is the fair value of the biological asset determined? | Costs and expenses (46.15%) | The cost approach is prioritized to valuation assets, although IAS 41 promotes the use of fair value, revealing a gap between standard and practice. |

| 7. How is the agricultural product (egg) valued? | Cost per tray (73.08%) | Most use practical methods such as unit cost per tray, which is useful for operational control but limited in terms of accounting accuracy for valuation. |

| 8. Is forced shedding conducted and how long is the production cycle extended? | Not performed (76.92%) | Most companies do not apply laying cycle extension processes, which can limit the economic use of the biological asset. |

| 9. From what age do birds acquire? | 1 day (84.62%) | Companies assume the complete biological cycle from its initial stage, which reinforces the need to keep accounting control from birth as established by IAS 41. |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2025 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Copyright: This open access article is published under a Creative Commons CC BY 4.0 license, which permit the free download, distribution, and reuse, provided that the author and preprint are cited in any reuse.