Submitted:

23 April 2025

Posted:

23 April 2025

You are already at the latest version

Abstract

This paper analyzes the impact of monetary policy on the structure of the banking market in Colombia, considering the recent period of an active monetary policy, in the context of high inflation rates. Using monthly credit portfolio data between 2017 and 2023, concentration indicators such as the Herfindahl-Hirschman Index (HHI), CRk indices, and the dominance index are estimated, and a VAR model is employed to evaluate the concentration response to a monetary shock. The results show that, although concentration levels remain high, they coincide with reducing the probability of market dominance. Also, monetary policy has a structural effect on market evolution, favoring consolidation in contractionary scenarios. The paper contributes to the debate on the non-neutrality of economic policy in contexts of high financial concentration and puts forward public policy recommendations to strengthen banking competition and financial inclusion.

Keywords:

Monetary policy

; banking concentration

; inflation

; VAR models

1. Introduction

The structure of financial markets, particularly the configuration of the banking sector, plays a key role in shaping the effectiveness and consequences of monetary policy.

Although studies on how bank concentration affects monetary policy transmission have abounded in recent decades (Adams & Amel, 2010; Baarsma & Vooren, 2018; Severe, 2016), less attention has been paid to the reverse causal relationship, i.e., whether monetary policy itself alters the structure of the banking sector by increasing or decreasing market concentration. This question has gained importance in light of the contractionary monetary interventions observed globally,

including in emerging markets such as Colombia, in response to post-pandemic inflationary shocks, where policy rates reached historically high levels and bank concentration is already high.

This paper addresses the research question: What is the effect of monetary policy on the level of bank concentration? It is based on emerging empirical evidence suggesting that monetary policy is not structurally neutral. Instead, by changing interest rates and affecting liquidity, central banks may unintentionally favor large and well-capitalized banks, thereby accelerating market consolidation and altering long-term financial dynamics (Jović, 2025). This phenomenon raises new concerns about the compatibility between monetary and competition policies, especially in small and middle-income economies.

To investigate this question, the study focuses on the Colombian banking sector, which provides a relevant context due to its stability, profitability, and relatively high concentration levels. Using monthly data on credit participation at the bank level, this paper constructs the values of the Herfindahl-Hirschman Index (HHI) between 2017 and 2023. It compares them against changes in the policy interest rate set by Banco de la República. The hypothesis is that expansionary monetary policy increases bank concentration over time, especially during macroeconomic stress or weak financial intermediation periods.

This research draws on multiple streams of literature. Severe (2016) finds that bank concentration reduces the responsiveness of credit to monetary policy and the sensitivity of industrial growth to interest rate changes. Their analysis of 22 OECD countries shows that a 1 % reduction in the monetary policy interest rate leads to significantly higher industrial growth in countries with lower bank concentration. Similarly, Baarsma and Vooren (2018) argue that competitive banking sectors facilitate a faster and more complete transmission of unconventional monetary policy. They point out that traditional measures such as the HHI often underestimate competitive pressures and suggest that market behavior, captured through indicators such as the Boone index or the Panzar-Rosse H-statistic, is a better predictor of policy effectiveness.

Jović (2025) examines whether monetary policy influences European banking structure in a more direct approach. He finds that prolonged low interest rates have increased concentration, particularly in economies with fragile banking sectors. His findings suggest a two-stage transmission mechanism: first, declining profitability of small and medium-sized banks; second, mergers and exits leading to increased market power of dominant institutions.

This paper adopts a similar analytical approach but focuses on the case of Colombia. The methodology consists of calculating monthly HHI scores from banks' market shares and modeling them as a function of the policy rate, controlling for inflation, credit growth, and macroeconomic trends. In doing so, the study aims to contribute to a more integrated understanding of monetary policy, assessing its short-term effects on inflation and output and its structural consequences on financial market concentration.

The findings of this paper have three important implications. First, they support the hypothesis that monetary policy can act as a structural force in financial markets by influencing concentration dynamics. Second, they highlight that the impact of monetary policy on concentration depends on the context, the initial market structure, regulatory capacity, and the degree of financial development. Third, the results point to a feedback loop: as bank concentration increases, the effectiveness of future monetary interventions may decrease, thus complicating macroeconomic stabilization efforts.

From a policy perspective, these results are particularly relevant for central banks acting as bank regulators. They suggest that monetary policy and competition policy should not be seen as isolated areas, but rather as interacting levers in the governance of financial systems. The potential for accommodative monetary stances to reduce competition in the long run calls for greater coordination between monetary authorities and financial supervisors.

This paper contributes to a growing body of research emphasizing monetary policy's non-neutrality concerning financial structure. It provides new empirical evidence from the Colombian case and encourages policymakers to incorporate market structure considerations in designing and evaluating monetary policy frameworks. It also contributes to the literature by analyzing the concentration and competitive dynamics of the Colombian banking sector using key market indicators such as the Herfindahl-Hirschman Index (HHI) to assess market concentration (Rhoades, 1993) and the Dominance Index to assess the presence of dominant firms (Melnik et al., 2008). Therefore, the rest of the paper is structured as follows: in the second section, the literature review, section 3 introduces the data and analysis techniques used in the study, and finally, some conclusions and policy implications.

2. Literature Review

The interaction between monetary policy and the structure of the banking sector has become increasingly relevant, especially in a context of constantly changing interest rates and the use of unconventional monetary policy instruments (NCMP). Recent literature highlights that the effectiveness of monetary policy transmission is not only influenced by the stance of central banks but also by the competitive and concentration dynamics within the banking system, and that monetary policy decisions can, in turn, affect the levels of competition in the banking system.

Determinants of Concentration in the Banking System

The structure of financial markets has been a central topic of economic research, especially in the context of bank concentration and its effects on competition, financial stability, and consumer welfare. The banking sector has unique characteristics that differentiate it from other sectors, such as high barriers to entry, network externalities, and strict regulatory oversight. Traditionally, banking competition has been analyzed through two opposing views: the structure-conduct-performance hypothesis (SCP) and the efficient structure hypothesis (ES) (Bain, 1951; Demsetz, 1973).

The SCP hypothesis postulates that higher concentration in the banking sector reduces competition, leading to higher placement rates, lower deposit rates, and lower financial inclusion (Berger & Hannan, 1989). In contrast, the ES hypothesis argues that concentration is due to increased efficiency, as larger banks achieve economies of scale and scope that allow them to offer better services and lower consumer costs (Berger, 1995). In addition, spatial competition models, such as Hotelling's (1929) model, have been widely used to analyze product differentiation and competition among banks (Salop, 1979). These models have been extended to include digital banking, emphasizing how neo banks and fintech firms disrupt traditional banking structures (Philippon, 2019)

Research in emerging markets, including Latin America, reveals that greater concentration correlates with increased financial exclusion and higher loan collateral requirements, particularly for SMEs. A concentrated banking market can significantly affect corporate financing. Studies have shown that firms in highly concentrated banking sectors often face higher collateral requirements, which can disproportionately affect small and medium-sized firms (Thein et al., 2024). In markets characterized by high concentration, financial institutions tend to exhibit risk-averse behavior, increasing the propensity to require collateral for SMEs and large corporations. Consequently, this increased concentration puts additional pressure on credit-seeking firms, limiting their ability to invest and expand. A comparative analysis of financial systems across Latin America suggests that bank concentration in Colombia is above the regional average, leading to increased barriers to credit access. Research by Cao-Alvira and Gómez-González (2025) on regional banking concentration in Colombia indicates that firms operating in highly concentrated banking environments tend to have higher accounting leverage, reflecting limited financing options.

The emergence of neobanks can disrupt traditional banking structures by offering low-cost digital financial services. Unlike traditional banks, neobanks operate without physical branches and leverage innovations in financial technologies to reach underserved populations. In Colombia, neobanks such as Nu and Lulo Bank have introduced services with reduced fees, simplified account-opening processes, and increased accessibility through mobile platforms (Frost, 2020). However, while neobanks provide greater financial inclusion, they also face regulatory challenges and infrastructure limitations that may hinder their ability to compete effectively with traditional banks. A study on competition in the banking sector in Latin America concluded that regulatory frameworks often favor established financial institutions, creating an uneven playing field for new entrants (Banco de la República de Colombia, 2022). In addition, research on the impact of FinTech on traditional banking suggests that while neobanks increase competition in deposit markets, their influence on banks' market power remains limited.

On the other hand, regulatory supervision plays a crucial role in shaping the competitive dynamics of the banking sector. Historically, the Colombian financial sector has undergone important transformations, including the financial liberalization reforms of the 1990s, which aimed to increase competition and improve market efficiency (Holmes et al., 2015). Despite these efforts, the country's banking market remains highly concentrated, with the three largest banks concentrating approximately 60% of total credit issuance. Research suggests that regulatory barriers limit market entry for smaller banks and FinTech firms. Strict capital requirements, licensing restrictions, and compliance costs create challenges for new entrants, reinforcing the dominance of traditional banks. Studies on banking regulation in Latin America emphasize the need for open banking initiatives, which could facilitate competition by allowing new entrants to access customer data from established financial institutions (Makhlouf et al., 2023).

The elasticity of substitution between traditional banks and neobanks provides a quantitative measure of how price, service, or other attributes affect the likelihood that consumers will switch from one type of bank to another. If the elasticity is high, neobanks represent a strong competitive force, exerting downward pressure on fees and interest rate spreads. If elasticity is low, traditional banks can retain their market power, allowing them to maintain higher fees and interest rates without significantly losing customers.

A key factor in the debate on monopolistic competition in the banking sector is financial inclusion. Despite advances in bankarization, a significant portion of the Colombian population remains unbanked or relies on informal financial services (Demirgüç-Kunt et al., 2021). Neobanks have the potential to close this gap by offering simplified digital banking solutions with minimal fees, allowing people without access to traditional banking services to participate in the formal financial system.

However, regulatory restrictions, lack of digital literacy, and limited financial education programs hinder the rapid adoption of these alternatives, especially in rural and low-income populations (Camara & Tuesta, 2017). Government policies promoting digital literacy and financial education will be crucial to ensure the widespread adoption of neobanks and fintech innovations (OECD, 2023). In addition, regulatory adjustments that enable greater interoperability among financial service providers could increase competition and improve consumer outcomes.

Empirical evidence suggests that the elasticity of substitution between traditional banks and neobanks is increasing, meaning that consumers are more willing to switch providers based on service quality, fees, and accessibility (Frost, 2020). The adoption of mobile banking services has grown significantly, especially among younger generations and urban populations (IMF, 2023).

However, the persistence of high switching costs, including regulatory requirements for account portability and reliance on traditional banking rails for transactions, limits the full exploitation of competitive advantages (Gomber et al., 2020). In addition, banks' control over digital payment infrastructure allows them to impose higher costs on neobanks, reducing their competitive advantage (World Bank, 2023).

However, traditional banks dominate the financial infrastructure, including payment networks, ATM access, and interbank transactions, making it difficult for neobanks to operate independently (Banco de la República de Colombia, 2021). Many new banks rely on

Partnerships with traditional banks for transaction processing can increase operational costs and dependence on traditional banks (González-Páramo, 2021).

In addition, consumer confidence in fully digital banks remains a challenge, as many users still prefer traditional banking institutions' perceived security and stability (Klapper et al., 2021). Although neobanks have lower costs and greater accessibility, concerns about cybersecurity, fraud, and gaps in financial literacy limit their adoption, especially among older and rural populations (World Economic Forum, 2022).

Monetary Policy and Bank Concentration

An important line of literature has studied the relationship between monetary policy and banking market structure. For example, Adams and Amel (2010) investigate whether increasing bank concentration in the United States has led to increased market power, concluding that, although consolidation has increased, it has not necessarily translated into greater pricing power. Their findings suggest that structural indicators, such as concentration ratios, may not fully reflect how consolidation affects bank behavior or market competition. This is important when assessing monetary policy transmission in increasingly concentrated markets.

In the context of the euro area, Baarsma and Vooren (2018) analyze how competition within the banking sector conditions the effectiveness of monetary policy, using a panel error correction model for 14 euro area countries, they show that in more competitive banking environments, the transmission of monetary policy-measured through the pass-through of monetary stimulus to long-term interest rates-is faster and more complete. They also highlight the inadequacy of traditional concentration measures (e.g., the HHI) to capture real competitive pressures. They propose using indicators such as the Boone indicator and the Panzar-Rosse H-statistic for more accurate assessments.

Building on these insights, Jović (2025) advances the debate by examining the reverse causal relationship: whether expansionary monetary policy affects bank concentration. His empirical analysis based on VARs and SCVs of 33 European countries between 2008 and 2020 shows that central bank policy rate cuts - in particular by the ECB - led to significant increases in bank concentration, especially in countries with low initial levels of profitability and weaker

Financial stability. This is known as the second wave of monetary policy effects: the first is a decline in profitability, and the second is a structural shift towards greater market concentration. In particular, the study finds evidence of monetary policy spillovers: ECB policy decisions significantly influenced concentration dynamics even in non-euro area countries such as Poland, Hungary, Bulgaria, and Serbia, where national monetary policies had weaker effects.

Severe (2016) empirically demonstrates that bank concentration significantly dampens the macroeconomic effects of monetary policy. Using panel data from 22 OECD countries on 59 manufacturing sectors, he finds that countries with more concentrated banking systems exhibit lower growth and respond less to interest rate changes. For example, a 100-basis-point reduction in interest rates boosts industrial growth by 0.049% at the average concentration level. However, the policy change almost doubles its effect when the concentration is 5% lower. Severe's study highlights that monopolistic or oligopolistic banking structures limit the effectiveness of monetary policy by reducing the elasticity of lending and investment responses. This idea extends and deepens the microeconomic inefficiency arguments by Berger and Hannan (1998).

Taken together, these studies paint a comprehensive picture of the dual role of bank concentration in the monetary transmission mechanism: on the one hand, it can dampen the responsiveness of lending rates to changes in monetary policy, as dominant banks may be less reactive to interest rate changes; on the other hand, monetary policies themselves can catalyze further concentration by disproportionately benefiting larger and more resilient banks. These findings raise important concerns about the long-term implications of low-interest rate environments, especially for the design of prudential regulation and coordination between monetary and financial stability policies.

This paper builds on these contributions to explore how market structure conditions banks' responsiveness to monetary impulses in Colombia, while considering whether changes in concentration may be a consequence of monetary policy, not just a moderator. The empirical analysis will apply dominance indices and concentration metrics over time, contextualizing the Colombian banking system within global monetary dynamics and offering new insights into how structure and policy co-evolve.

3. Data and Methods

The methodological strategy is divided into two parts. In the first part, we explore the structure of the banking market in Colombia by estimating different measures that allow us to approximate the degree of concentration of the banking system. In the second part, we will identify the effects of monetary policy on the degree of concentration of the banking system in Colombia by applying VAR and VEC models.

3.1. Data

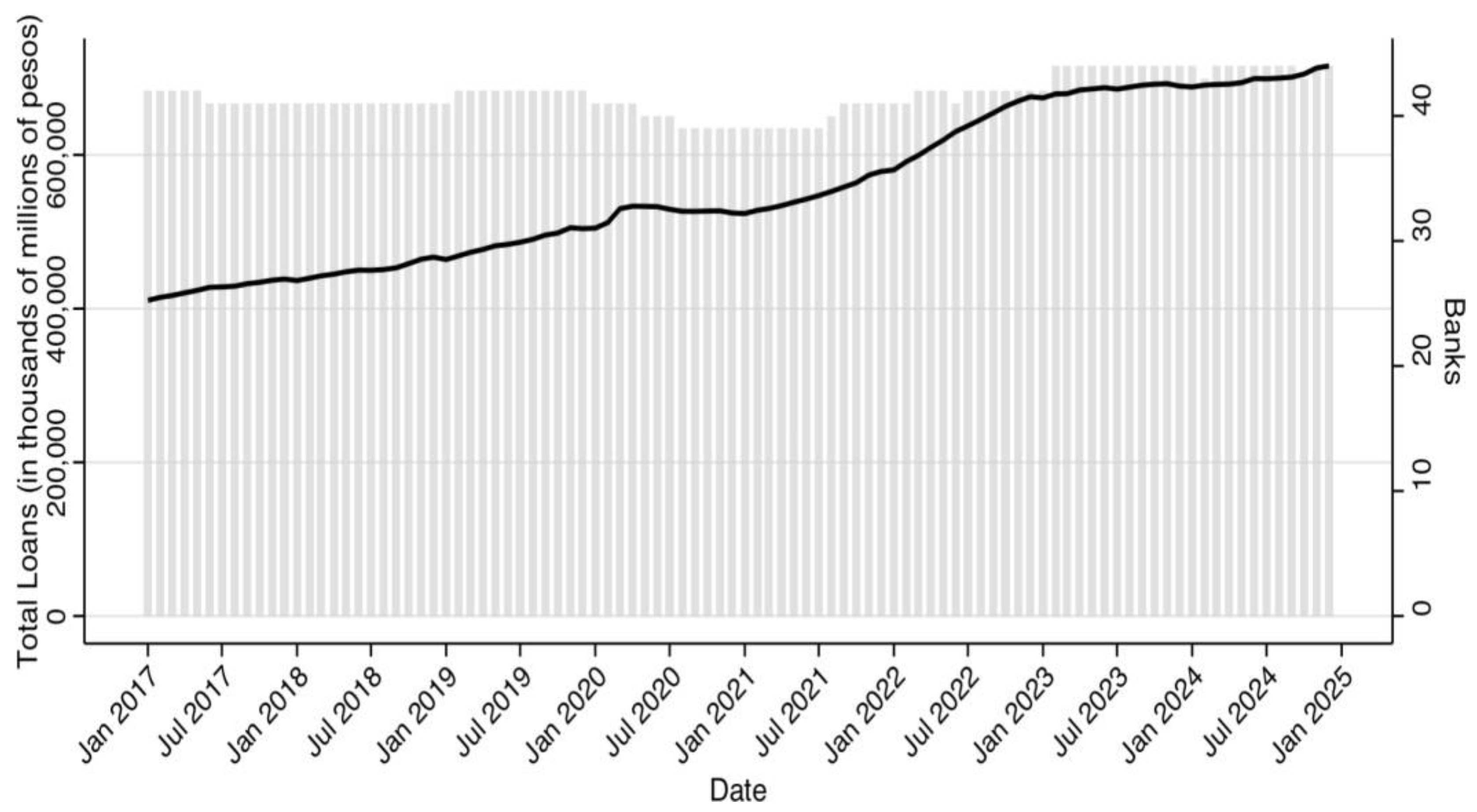

In order to approximate the measurement of the degree of concentration of the credit product in the Colombian financial system, data have been collected from the Financial Superintendency of Colombia. This entity oversees the operations of banks in the country. The data obtained provides information on the total portfolio, the balance in arrears, the balance at risk, and the written-off balance for each credit establishment from 2017 to 2024. Figure 1 shows the total portfolio evolution (black line) versus the number of establishments (bars) and allows for the observation of an increasing trend in the portfolio, evidencing an expansion of the credit and assets of the establishments in this period. As for the establishments, a stability in their number can be observed. This could indicate that lending activity could be dominated by a few large institutions as the portfolio grows and the number of establishments changes significantly.

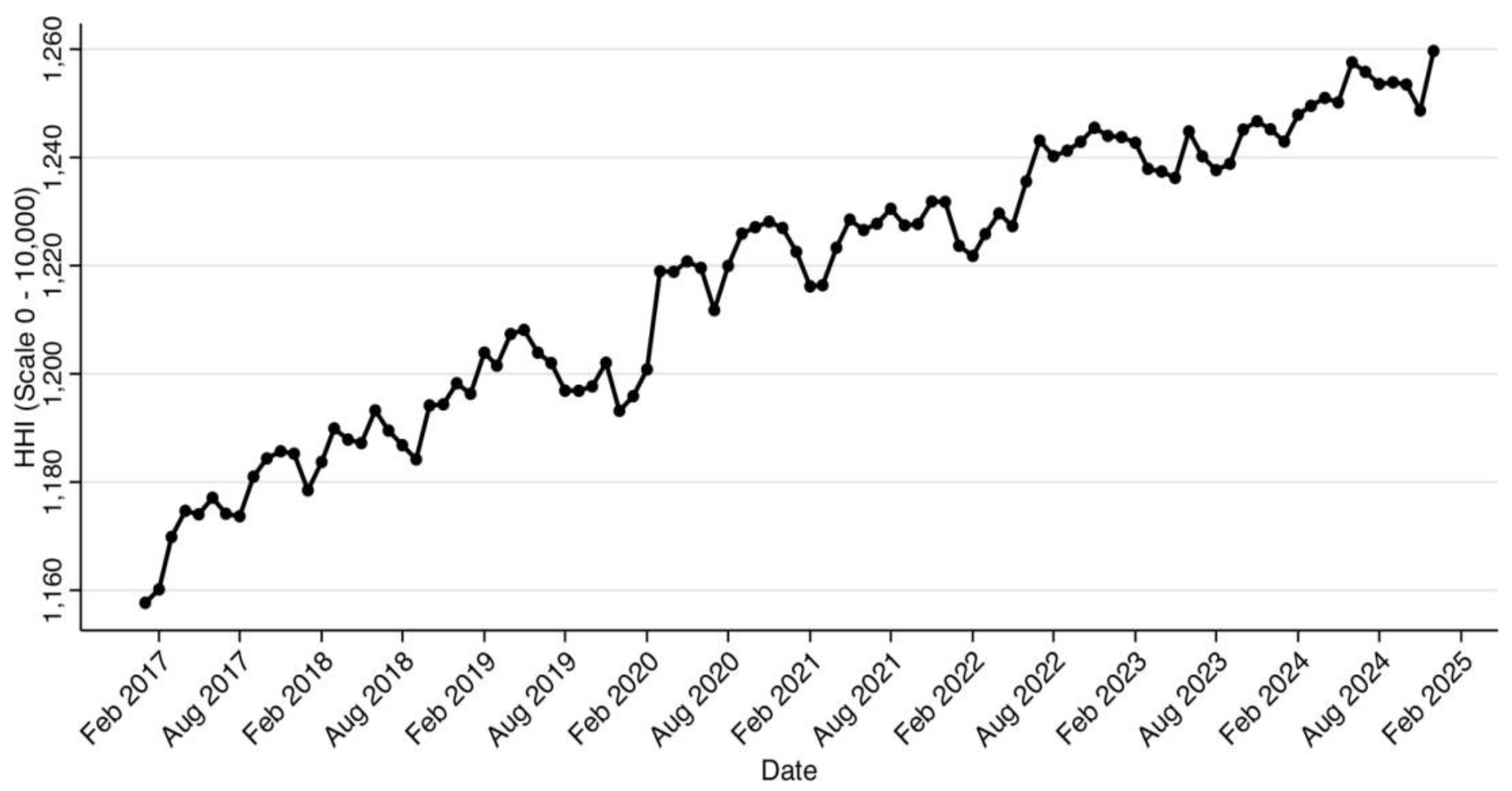

Secondly, an approximation to the measurement of market concentration in the banking sector has been made using the Herfindahl-Hirschman Index (HHI), which sums the squared market shares of all the companies in the market:

where si is the market share of the establishment i. A high HHI indicates higher concentration, suggesting a more monopolistic market structure, while a low HHI suggests a more competitive market (Rhoades, 1993). Empirical studies show that concentration in the financial sector varies significantly across countries. For example, Cetorelli and Gambera (2001) conclude that higher concentration in banking markets correlates with lower credit availability for small and medium-sized enterprises (SMEs). Similarly, Beck, Demirgüç-Kunt and Levine (2006) argue that excessive concentration reduces financial inclusion and innovation, as dominant banks face less competitive pressure to innovate. Figure 2 presents the results for the Colombian market. A growing trend can be observed, suggesting that the leading financial institutions in the country have been consolidating their market share.

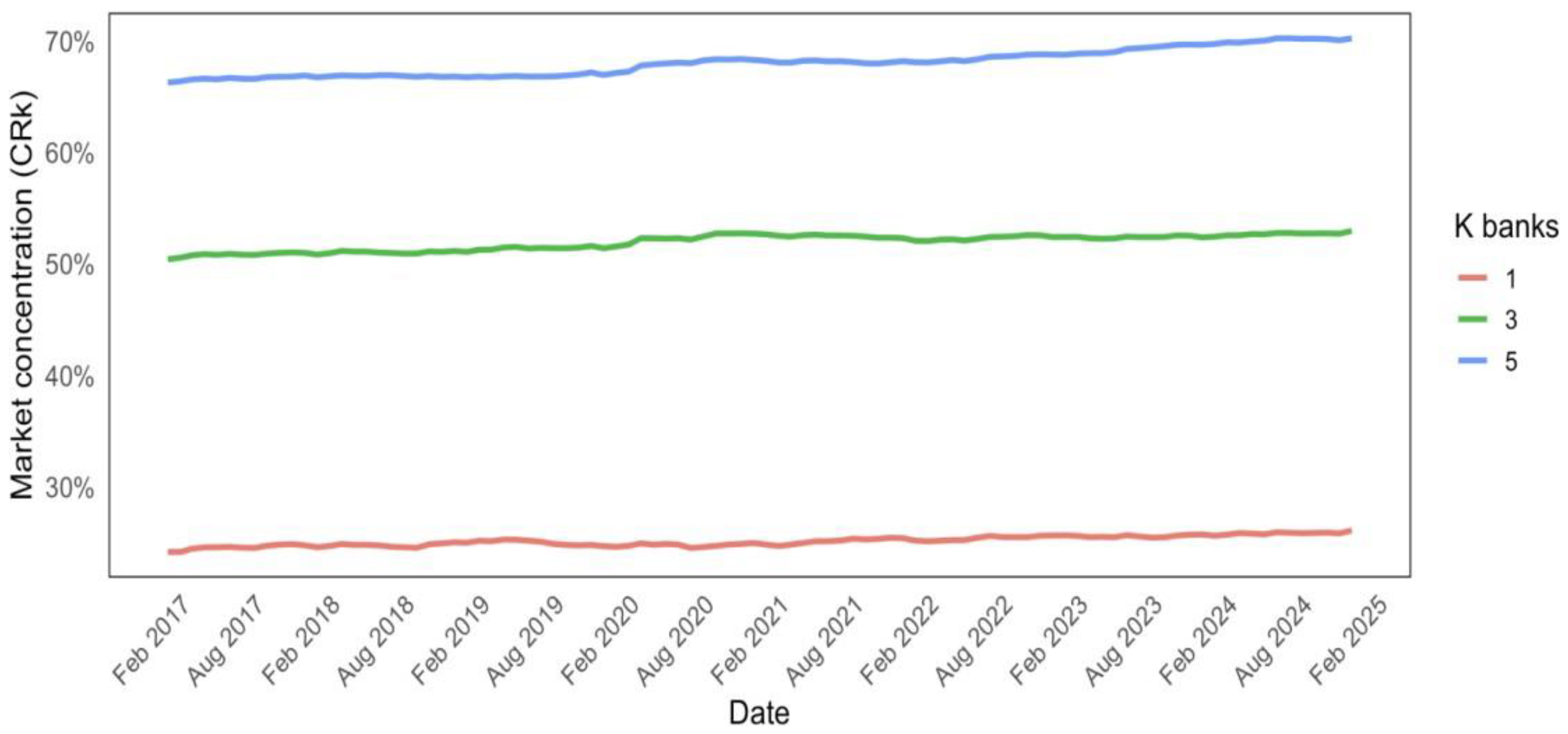

An alternative measure of concentration is the CRk (k-firm concentration ratio): It measures the combined market share of the k largest banks. Figure 3 shows the results of this.

The indicator for the Colombian market uses the three most significant and the five largest banks. The increasing market concentration observed in the Colombian financial sector, especially among the top five institutions (CR5), suggests a progressive consolidation of market power. While the CR1 and CR3 indicators show relatively stable values, the gradual increase in CR5 indicates that a handful of institutions are capturing a larger share of total lending activity. This trend raises concerns about reduced competition, as greater concentration may lead to higher borrowing costs, less financial product innovation, and limited access to credit for SMEs and low-income consumers. However, a concentrated banking system can improve financial resilience from a stability perspective, as dominant banks typically have greater regulatory oversight and capital buffers. The policy challenge lies in balancing competition and stability, ensuring that new market entrants such as neobanks and fintechs can operate on a level playing field while maintaining a sound financial system. Future research should assess whether regulatory frameworks foster or hinder competition, particularly in digital banking and alternative lending markets.

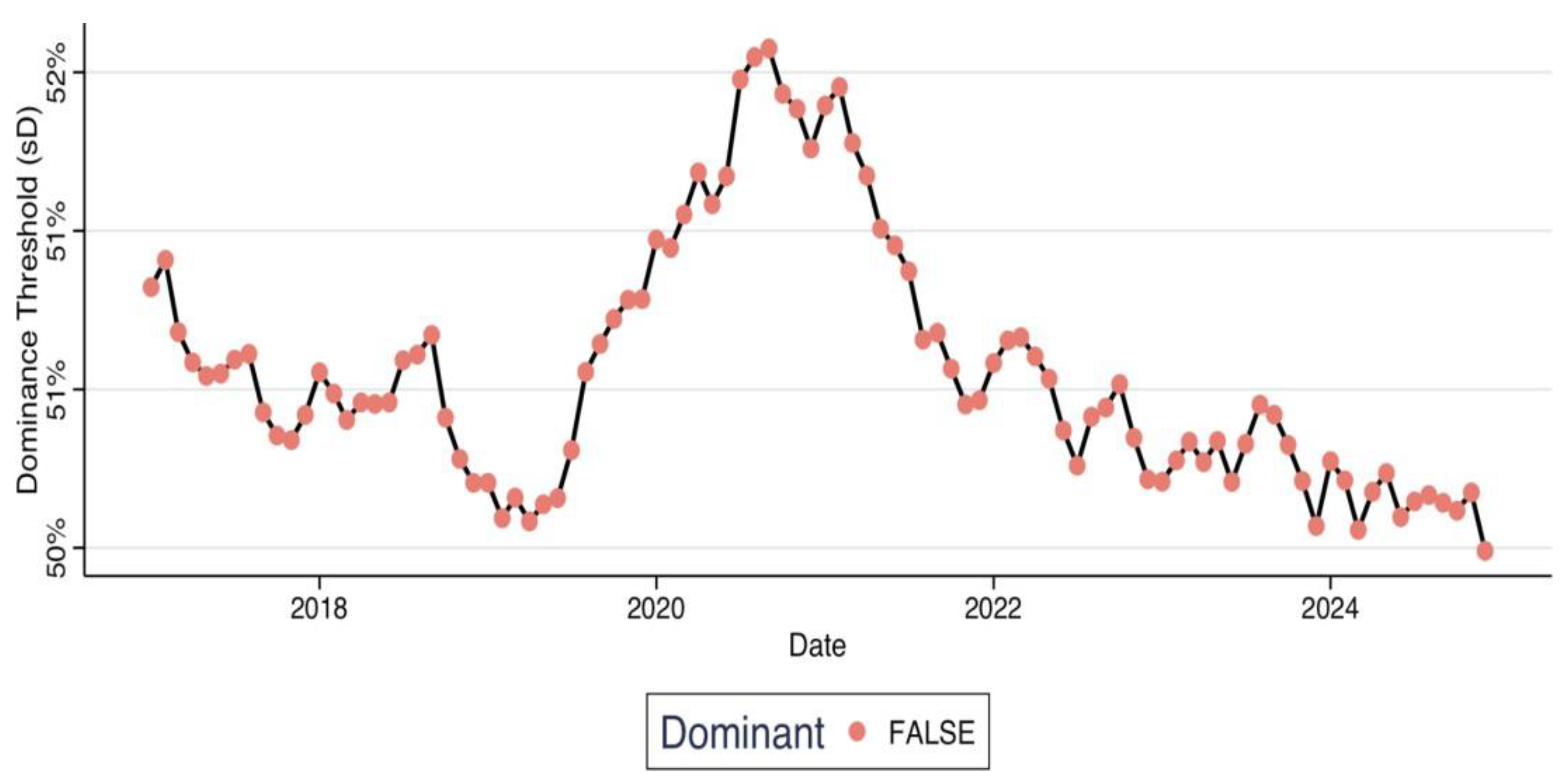

Following Melink et al (2008), an endogenous threshold has been estimated to determine when a firm or several firms occupy a dominant position in the market. Unlike traditional measures of concentration, such as the HHI index, this approach focuses on assessing the relative market power of the largest firm(s) as a function of the industry's competitive structure. Specifically, in this case, taking into account what has been observed in the

Concentration measures, the dominance index has been calculated considering the five largest firms and is defined as follows:

where s1 represents the share of the largest establishment, s2−5 is the sum of the shares of the following four most prominent firms, s6−N corresponds to the total share of the other firms in the market, andγ is a parameter that captures the intensity of potential competition; in this case, a value of 1 has been used. The index structure allows adjusting the definition of dominance according to market conditions. If the gap between the leading establishment and its direct competitors is high, the dominance threshold decreases, which implies a stricter criterion to be considered dominant. Figure 4 shows the results for the Colombian case in the period analyzed. The vertical axis shows the concentration threshold to be considered dominant in the market, and the line shows the behavior of the index and the red dots, the years in which the threshold has not been exceeded.

It is observed that the dominance threshold (sD) has varied, reaching a peak around 2020 and subsequently decreasing, coinciding with the appearance of the first neobank in the Colombian market (Lulo Banco), without returning to the initial levels. This suggests that, although the dominance threshold has fluctuated, no institution has surpassed this threshold in the years analyzed, and that the probability of this occurring, with the emergence of the neobanks, has been reduced.

3.2. Monetary Policy and Bank Concentration

In order to analyze the dynamic relationship between banking market concentration and monetary policy in Colombia, a reduced-form vector autoregressive (VAR) model is estimated using monthly data from the financial system. The model includes three endogenous variables: the Herfindahl-Hirschman Index (HHI) as a proxy for bank concentration, the nominal monetary policy rate set by Banco de la República, and the consumer price index (CPI) inflation rate. Before estimating the VAR model, stationarity tests were performed using a simplified version of the Dickey-Fuller test. The results indicated that the bank concentration index (HHI) and the monetary policy rate were not stationary in levels, so they were transformed to first differences. Subsequently, VAR models with lags between 1 and 6 were estimated, and the Akaike information criterion (AIC) was used to select the optimal specification. The minimum value of the AIC was obtained with five lags, a decision that guides the final model estimation and impulse-response analyses. Therefore, the specification of the estimated equations is as follows:

5 5 5

∆𝐻𝐻𝐼𝑡 = 𝛼1 + ∑ 𝛽1𝑖 ∆𝐻𝐻𝐼𝑡−𝑖 + ∑ 𝛾1𝑖 ∆𝑀𝑜𝑛𝑒𝑡𝑎𝑟𝑦_𝑝𝑜𝑙𝑖𝑐𝑦𝑡−𝑖 + ∑ 𝛿1𝑖 ∆𝐼𝑛𝑓𝑙𝑎𝑡𝑖𝑜𝑛𝑡−𝑖 + 𝜀1𝑡

𝑖=1

5 5 5

∆𝑀𝑜𝑛𝑒𝑡𝑎𝑟𝑦_𝑃𝑜𝑙𝑖𝑐𝑦𝑡 = 𝛼1 + ∑ 𝛽1𝑖 ∆𝐻𝐻𝐼𝑡−𝑖 + ∑ 𝛾1𝑖 ∆𝑀𝑜𝑛𝑒𝑡𝑎𝑟𝑦𝑃𝑜𝑙𝑖𝑐𝑦𝑡−𝑖 + ∑ 𝛿1𝑖 ∆𝐼𝑛𝑓𝑙𝑎𝑡𝑖𝑜𝑛𝑡−𝑖 + 𝜀1𝑡

𝑖=1

5 5 5

∆𝑖𝑛𝑓𝑙𝑎𝑡𝑖𝑜𝑛𝑡 = 𝛼1 + ∑ 𝛽1𝑖 ∆𝐻𝐻𝐼𝑡−𝑖 + ∑ 𝛾1𝑖 ∆𝑀𝑜𝑛𝑒𝑡𝑎𝑟𝑦_𝑝𝑜𝑙𝑖𝑐𝑦𝑡−𝑖 + ∑ 𝛿1𝑖 ∆𝐼𝑛𝑓𝑙𝑎𝑡𝑖𝑜𝑛𝑡−𝑖 + 𝜀1𝑡

𝑖=1

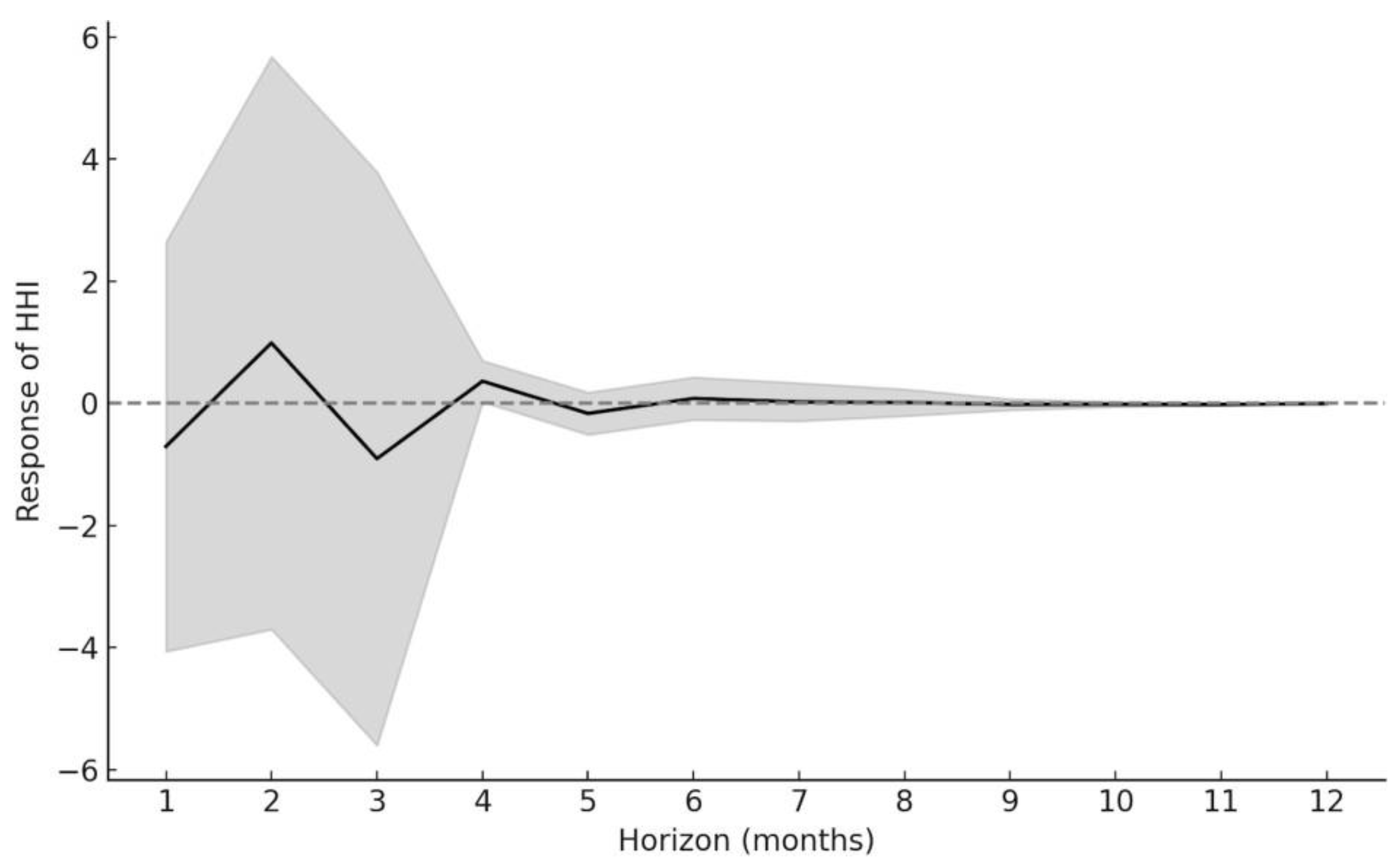

Once the VAR model was estimated, we proceeded to simulate impulse-response functions (IRF) to track the effect of a unit exogenous shock to the monetary policy rate on the HHI index over a 12-month horizon. The IRF is calculated recursively from the estimated coefficients, assuming that only the monetary policy variable receives a shock in the initial period, while the others remain unperturbed. The confidence intervals are constructed using the delta method, which allows the standard errors of the estimated coefficients to be propagated along the recursive system, providing an approximation to the uncertainty associated with the dynamic response. This methodology allows us to examine the direction, magnitude, and persistence of the effect of monetary policy on bank concentration. It contributes to understanding how monetary cycles may affect competition in the Colombian banking sector.

Figure 5.

Impulse Hhi's response to the Monetary Policy shock.

4. Discussion

The Colombian financial sector has high concentration levels, with a few dominant institutions controlling most credit services. The Herfindahl-Hirschman Index (HHI) and concentration indices (CR3, CR5) indicate that market concentration has remained persistently high, reinforcing concerns about limited competition. Although the sector has expanded in absolute terms, the distribution of credit remains skewed toward a few large institutions, which could limit access to credit for small businesses and underserved populations.

From the monetary policy approach, the simulation of impulse-response functions reveals that a contractionary shock in the intervention rate hurts the HHI concentration index, which could be interpreted as an incentive to competition. However, this effect is neither linear nor immediate and is conditioned by the initial degree of concentration. In other words, monetary policy can act as a structural force, but its impact varies depending on the configuration of the financial system. This evidence supports the thesis that monetary policy is not neutral to market structure, and that its design should consider its effects on competition. It supports the evidence in the literature, which argues that periods of monetary policy easing favor large banks in deepening concentration conditions. Consequently, greater coordination between monetary authorities and financial system regulators is recommended to align macroeconomic stability objectives with competition and market efficiency principles.

References

- Bank of the Republic of Colombia (2021). Financial Stability Report 2021. Bogotá, Colombia.

- Camara, N., & Tuesta, D. (2017). Measuring financial inclusion: A multidimensional index. BBVA Research.

- Claessens, S., Frost, J., Turner, G., & Zhu, F. (2021). Fintech credit markets worldwide: Size, drivers, and policy issues. BIS Quarterly Review.

- Dixit, A. K.; Stiglitz, J. E. Monopolistic competition and optimum product diversity. The American Economic Review 1977, 67, 297–308. [Google Scholar]

- Frost, J. (2020). The economic forces driving fintech adoption across countries. BIS Working Papers.

- OECD (2023). Digital financial literacy: Empowering consumers in a digital age. Paris, France. World Bank (2023). Fintech and the future of finance: Trends, risks, and regulatory responses. Washington, DC.

- Banco de la República de Colombia (2022). Structure and concentration of the financial sector in Colombia.

- Beck, T.; Demirgüç-Kunt, A.; Levine, R. Finance, inequality, and the poor. Journal of Economic Growth 2007, 12, 27–49. [Google Scholar] [CrossRef]

- Berger, A. N., Demsetz, R. S., & Strahan, P. E. (2004). The consolidation of the financial services industry: Causes, consequences, and implications for the future. Journal of Banking & Finance, 23(2-3), 135-194. [CrossRef]

- Buchak, G.; Matvos, G.; Piskorski, T.; Seru, A. Fintech, Regulatory Arbitrage, and the Rise of Shadow Banks. Journal of Financial Economics 2018, 130, 453–483. [Google Scholar] [CrossRef]

- Cao-Alvira, J. J., & Gomez-Gonzalez, J. E. (2025). On Regional Bank Concentration and Firm Leverage: The Case of Colombia. Emerging Markets Finance and Trade, 61(1), 80-93. [CrossRef]

- Claessens, S.; Laeven, L. What drives bank competition? Some international evidence. Journal of Money, Credit and Banking 2004, 36, 563–583. [Google Scholar] [CrossRef]

- Degryse, H.; Ongena, S. Distance, Lending Relationships, and Competition. Journal of Finance 2005, 60, 231–266. [Google Scholar] [CrossRef]

- Frost, J. (2020). The economic forces driving fintech adoption: Evidence from banking data. BIS Working Papers.

- Gambacorta, L., Ricci, M., & Vandone, D. (2020). Price and Non-Price Competition in the Fintech Era. BIS Working Paper.

- Holmes, M. J., Otero, J., & Panagiotidis, T. (2015). On the dynamics of banking concentration and financial development. The Economic Journal, 125(582), 1073-1096.

- Makhlouf, H.; Gray, D.; Cooper, B. Banks, financial markets, and income inequality: Evidence from emerging economies. International Journal of Finance & Economics 2023, 28, 3185–3203. [Google Scholar]

- Matsumoto, A.; Merlone, U.; Szidarovszky, F. The Herfindahl-Hirschman Index as a Measure of the Degree of Market Power. Economic Modelling 2012, 29, 2343–2349. [Google Scholar]

- Philippon, T. The FinTech Disruption: Innovation, Regulation, and the Future of Banking. American Economic Review 2019, 109, 2132–2163. [Google Scholar]

- Rhoades, S. A. (1993). The Herfindahl-Hirschman Index. Federal Reserve Bulletin, 79(3), 188-189.

- Tirole, J. (1988). The Theory of Industrial Organization. MIT Press.

- Vives, X. (2016). Competition and Stability in Banking. Princeton University Press.

- World Bank (2020). Global Financial Development Report: Bank Regulation and Supervision.

Figure 1.

Total portfolio and number of institutions with credit activity supervised by the Superintendencia Financiera de Colombia.

Figure 1.

Total portfolio and number of institutions with credit activity supervised by the Superintendencia Financiera de Colombia.

Figure 2.

HHI for the banking system in Colombia.

Figure 3.

Concentration ratios CR1, CR3, and CR5 for the Colombian credit market.

Figure 4.

Leverage index for the credit market in Colombia.

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2025 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Copyright: This open access article is published under a Creative Commons CC BY 4.0 license, which permit the free download, distribution, and reuse, provided that the author and preprint are cited in any reuse.